Can I sell my pension?

Technically you can’t sell your pension, however you can release cash early from your pension. If you are thinking about selling your pension, then you should consider Pension Release, also known as Pension Unlocking or even Pension Surrender . This guide refers to these when mentioning selling a pension.

Should I transfer out of a defined benefit pension?

The Financial Conduct Authority (FCA) and the Pensions Regulator (TPR) believe that it will be in most people’s best interests to keep their defined benefit pension. If you transfer out of a defined benefit pension, you can’t reverse it.

What is a defined benefit pension?

A defined benefit or DB pension (also known as a final salary pension) is a special type of workplace pension. Instead of building up a pension pot over time, it provides you with a guaranteed annual income for life, based on your final or average salary (hence the name).

Can I ‘trade in’ a DB pension for a fixed-size pension?

You can ‘trade in’ a DB pension for a fixed-size pension pot of the kind found in defined contribution (DC) pensions. This is known as a final salary pension transfer (or defined benefit pension transfer).

Can you cash out a defined benefit pension?

Defined Benefit Plan Distributions In general, benefits are not paid until the Plan's specified retirement age. This often is age 62 or 65. However, many small Plans allow the participant to "cash out" their benefit, regardless of age, by electing a lump sum distribution in lieu of annual lifetime payments.

Can you take a lump sum from a defined benefit pension?

Taking your defined benefit pension as a lump sum You might be able to take your whole pension as a cash lump sum. If you do this, up to 25% of it will be tax-free, and you'll have to pay Income Tax on the rest.

Can you sell pension for a lump sum?

Pension plans and retirement annuities can be sold partially or fully for a cash lump sum. Income received after selling your pension plan depends on whether the money comes from a personal or occupational pension. Selling your pension plan typically requires proving you have an active life insurance policy.

Can I request a pension buyout?

If your company is offering to buy out your pension, they're offering you an opportunity to take your pension value as of a certain date in exchange for relief from the company's obligation to pay this in the future. It can take the form of an annuity, or more commonly, a one-time, lump-sum payment.

Can I take 25% of my DB pension?

Remember that you can withdraw a 25% cash lump sum from your final salary tax-free, but again even working out what constitutes 25% of your DB pension isn't a simple calculation.

What happens to my defined benefit plan if I leave the company?

If the plan you are leaving is a defined benefit plan, you would be notified of the amount that your reduced pension benefit would be.

Can I sell my pension before 55?

If you're under the age of 55, selling or withdrawing your pension in most circumstances is highly inadvisable. This is because you'll be hit with a huge 55% tax bill on the amount of cash you withdraw.

How can I avoid paying tax on my pension lump sum?

Ways to reduce tax on your pension however include:Not withdrawing more than you need from your pension each year.Utilising a drawdown scheme so that you can vary your yearly pension income.Taking out small pension pots in one lump sum to benefit from 25% being tax free.Avoid drawing large pensions in one go.More items...•

How do I sell my pension?

No, you cannot simply sell your pension. Your options for a defined contribution pension are to purchase an annuity, enter drawdown or access the cash it holds. You cannot sell a defined benefit pension either.

What is a typical pension buyout?

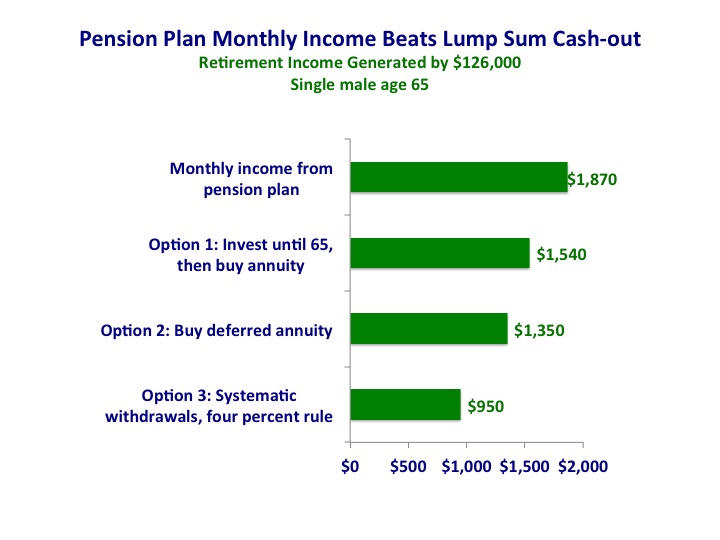

Keep in mind that a pension, in essence, pays you back your own money. You can withdraw 5% per year from any lump sum, even if the funds are earning nothing. Conservatively speaking, your money should last 20 years (5% x 20 = 100% withdrawal). Twenty years is a long time, especially if you're around age 65.

What is a good monthly retirement income?

But if you're able to supplement your retirement income with other savings or sources of income, then $6,000 a month could be a good starting point for a comfortable retirement.

What is Sell My Annuity LLC?

Sell My Annuity LLC exists to help the owner of an annuity or structured settlement annuity to determine if a lumpsum of cash today is better for their needs then small period structured settlement or annuity payments made over time.

Can you sell your pension and receive a settlement?

You are able to retain some pension payments as well as sell a portion off for a lump sum cash amount today. You are able to sell your pension and receive a cash settlement up front, but that does not mean you must sell your entire pension. If you only want to sell a portion of it, say $50,000 that is possible as well.

What happens to pension after selling?

To a certain extent, there is much more choice in how the income will be paid from a personal pension compared with an occupational scheme.

What happens if you release your pension early?

If you release all your money from your pension early you will not have anything left to provide you with income in retirement. Usually 25% of your pension can be released tax-free, the balance is taxed at your marginal rate at the time of release, this marginal tax rate could change in the future. GET STARTED TODAY.

Can you sell your pension before retirement?

Selling your pension prior to your pensionable age would usually result in a reduced income during retirement. If you are thinking about selling your pension, you can take part or all of your pension as a cash lump sum.

Does taking pension early reduce your income?

This service only applies to pensions in the UK. Taking benefits early will almost certainly reduce your pension income in retirement and is only suitable for a limited number of people and circumstances. This should not be seen as an easy option for raising cash.

Can you sell your pension?

Technically you can’t sell your pension, however you can release cash early from your pension. If you are thinking about selling your pension, then you should consider Pension Release, also known as Pension Unlocking or even Pension Surrender . This guide refers to these when mentioning selling a pension.

Can you sell your pension lump sum?

Please note that the tax treatment would depend upon your personal circumstances and may be subject to change in the future. Selling your pension, whether through cashing in an occupational or personal pension, still usually gives you the option to take a cash sum as well as income. This tax free cash sum is known as the Pension Commencement Lump ...

Why would I sell my pension?

Despite the fact that selling your pension almost always means less money in your pocket in the long run, many people choose to do it anyway. Often, they are in desperate need of a large sum of cash to pay for things like medical expenses, job loss, and other difficult situations.

What can go wrong?

The hard truth is that selling your pension payments for cash is usually not the best idea. The fact that your lump sum payment will be less than the combined payments you’re giving up means that the math just isn’t on your side.

Does this ever work out well?

Like anything, there are times when cashing out your pension might make more sense.

What is defined benefit pension?

Traditionally, defined benefit (DB) pensions have been seen as the gold standard when it comes to retirement saving. These pensions are provided by your employer’s pension scheme, and are determined by your years of service and either your final salary or your career average with the firm. So for example, each year you might accrue 1/60th ...

Can you take out a defined contribution pension?

Instead, employers will generally look for you to take out a defined contribution (DC) pension, where you, the employer and the Government all contribute a set amount. This money is then invested, which you can eventually use to buy an annuity that will deliver an income for life, or else keep it in invested.

What is a plan A?

EXAMPLE 1. Plan A is a defined benefit plan that covered both HCEs and NHCEs for most of its existence. The employer decides to wind up its business. In the process of ceasing operations, but at a time when the plan covers only HCEs, Plan A is amended to increase benefits and thereafter is terminated.

Is the sale of stock more advantageous to the seller or the purchase of assets?

Naturally, there are several variations of this type of arrangement, but they all usually lead back to the same questions and answers shown above. The sale of stock is usually more advantageous to the seller, while the purchase of assets is usually more favorable to the buyer.

Can a prior owner provide consulting services to a buyer?

If the prior owner agrees to provide consulting services to the buyer , then it is possible that the prior owner will now have a new sole proprietorship that will be receiving that consulting income, or he could set up a new entity solely for his consulting services. This leaves you with two possibilities.

Can a new entity sponsor a consulting plan?

The new entity that is receiving the consulting income could sponsor a plan, but you have to be careful that the relationship between the new entity and the original business is not such that it creates an affiliated service group.

Is a sale of stock a long term capital gain?

If the business was operated through a corporation (or an LLC taxed as a corporation) and the corporation was sold rather than the assets, the business and the corporation continue, just with new shareholders. The sale of stock will usually be a long-term capital gain to the seller; after the sale, the prior owner no longer has an operating entity ...

Does the buyer have to assume liabilities prior to a sale of a business?

With the sale of assets, the buyer gets to depreciate the assets purchased, making the purchase less expensive for the buyer, and the buyer does not have to assume any liabilities associated with the business prior to the purchase except as negotiated through the selling agreement.

Can you use past service and compensation for benefit accruals?

While there are certainly excellent arguments for not using past service and compensation for benefit accruals in such a plan — most of which are persuasive — ultimately, being able to substantially increase first-year funding for the plan may override the concern for any associated IRS audit risk.

What is defined benefit pension?

A defined-benefit pension plan requires an employer to make annual contributions to an employee’s retirement account. Plan administrators hire an actuary to calculate the future benefits that the plan must pay an employee and the amount that the employer must contribute to provide those benefits. The future benefits generally correspond ...

How much does a defined benefit plan pay?

One type of defined-benefit plan might pay a monthly income equal to 25% of the average monthly compensation that an employee earned during their tenure with the company. 3 Under this plan, an employee who made an average of $60,000 annually would receive $15,000 in annual benefits, or $1,250 every month, beginning at the age of retirement (defined by the plan) and ending when that individual died.

How does a straight life annuity work?

In a straight life annuity, for example, an employee receives fixed monthly benefits beginning at retirement and ending when they die. The survivors receive no further payments. In a qualified joint and survivor annuity, an employee receives fixed monthly payments until they die, ...

What is future benefit?

The future benefits generally correspond to how long an employee has worked for the company and the employee’s salary and age. Generally, only the employer contributes to the plan, but some plans may require an employee contribution as well. 1 To receive benefits from the plan, an employee usually must remain with the company for ...

How often do you get a pension payment?

Generally, the account holder receives a payment every month until they die. Companies cannot retroactively decrease benefit amounts for defined-benefit pension plans, but that doesn't mean these plans are protected from failing.

How long do you have to work to get a fixed benefit?

In most cases, an employee receives a fixed benefit every month until death, when the payments either stop or are assigned in a reduced amount to the employee’s spouse, depending on the plan.

When can defined benefit plans make in service distributions?

The IRS also notes that defined-benefit plans generally may not make in-service distributions to participants before age 62, but such plans may loan money to participants. 1 .

Choose a Defined Benefit Plan

Defined benefit plans provide a fixed, pre-established benefit for employees at retirement. Employees often value the fixed benefit provided by this type of plan. On the employer side, businesses can generally contribute (and therefore deduct) more each year than in defined contribution plans.

Hybrid Plans

Hybrid Plans phone forum (November 23, 2010) ( transcript PDF) - new hybrid plan regulations ( handout PDF)

Funding-based benefit restrictions

Funding-Based Benefit Restrictions - (February 23, 2012) ( transcript PDF) ( handout PDF)

What happens to defined contribution pension if you die?

There is a risk that there’s no money left in the pension when you die, especially if the pension needs to provide an income to your widow/widower after your death.

When does defined benefit stop?

Your defined benefit pension income will stop when you and any financial dependants die. In most cases this means that when you (and any financial dependants such as your widow/widower) die, your pension dies with you. And there is nothing to pass on to your family.

What is PPF compensation?

However, this type of scheme is usually protected by the Pension Protection Fund (PPF). The PPF might step in and pay members' retirement income as compensation if employers become insolvent and the scheme doesn’t have enough funds to pay their benefits.

What is pension increase conversion?

This is called a pension increase exchange or pension increase conversion. If you accept the offer, your pension will be paid at the new rate for the rest of your life – but without, for example, any future annual increases. This could reduce the purchasing power of your money due to inflation.

What happens when you transfer to a defined contribution scheme?

If you transfer to a defined contribution scheme, you’re giving up a guaranteed income for life that usually increases to help protect against the effects of inflation, for a future income that can't be predicted with any certainty.

Can you pass on your pension to your family?

In most cases this means that when you (and any financial dependants such as your widow/widower) die, your pension dies with you. And there is nothing to pass on to your family. But any money left in a defined contribution pension can be inherited by whoever you choose.

Is it bad to transfer out of a defined benefit scheme?

At a glance. In most cases, you’re likely to be worse off if you transfer out of a defined benefit scheme to a defined contribution scheme. This is even the case if your employer gives you an incentive to leave. The Financial Conduct Authority (FCA) and the Pensions Regulator (TPR) believe that it will be in most people’s best interests ...

What is defined benefit pension?

A defined benefit or DB pension (also known as a final salary pension) is a special type of workplace pension. Instead of building up a pension pot over time, it provides you with a guaranteed annual income for life, based on your final or average salary (hence the name). DB pensions are most often provided by the public sector (health, ...

Who provides DB pensions?

DB pensions are most often provided by the public sector (health, education etc) and government employers. Some private sector employers do still offer them, however. Historically they have been seen as a very attractive kind of pension.

What is a final salary pension transfer?

In a final salary pension transfer, your pension provider may offer you a certain amount of money in exchange for giving up your guaranteed pension for life. This money won’t be in the form of cash, but something called the ‘Cash Equivalent Transfer Value’ ...

How long can you withdraw £12,000 a year?

You can see that even with no growth at all, you could withdraw £12,000 a year from £300,000 for 25 years. If you were to achieve a mere 1 per cent average growth on your pension pot, you could withdraw £12,000 a year for over 28 years before your money ran out.

Is a DB pension more generous?

DB pensions are often seen as more generous, because it would take an above-average defined contribution (DC) pot to be able to buy an annuity that pays you the same amount as a DB scheme. What’s more, the payouts from a DB pension are guaranteed for the rest of your life.

Can a stock market crash affect your pension?

But a stock market crash can seriously dent the size of your pot in the short term, which can affect both the size of your income and the lifespan of your pension savings.

Does the PPF guarantee pension?

However, there may be a limit to how much the PPF can guarantee.