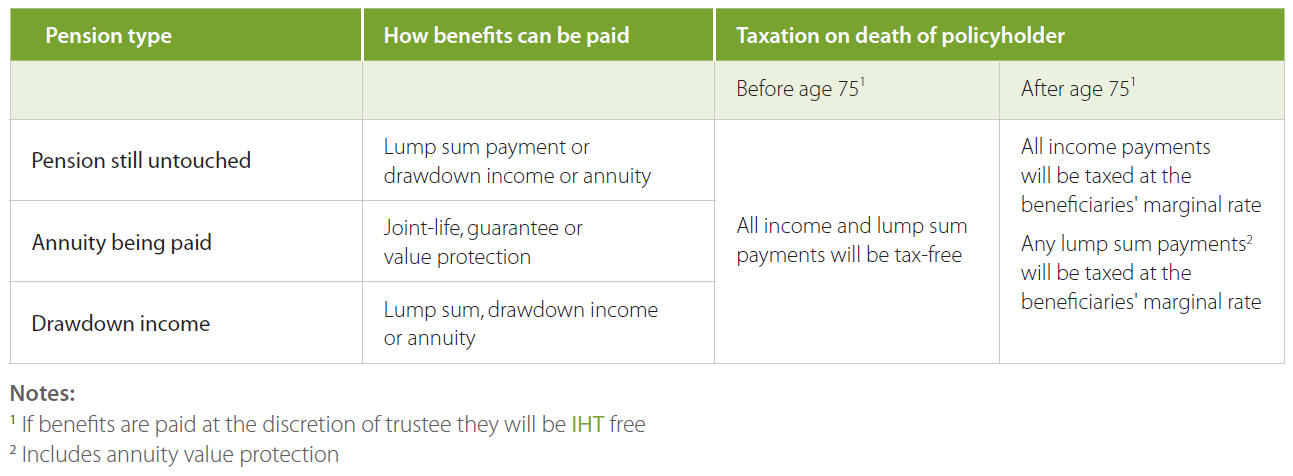

How are death benefits paid out?

Death benefits can be paid out as lump sums either immediately or at some future date, or they might be paid out in installments over time, as is the case with annuities. The primary question is: How do the types of death benefits and the methods of payout affect the taxes of beneficiaries?

Is a death benefit taxable?

No, a death benefit is not taxable. You will, however, still want to report it, but not with your gross income. What is a Death Benefit? A death benefit is the purpose of your life insurance policy—when you, the policyholder, pass away, a predetermined amount of money, known as the death benefit, is passed on to your beneficiaries.

Can a person with a disability receive a death benefit?

Also, those with a disability may experience issues with their Social Security disability benefits because the death benefit may be considered part of their income. Bottom Line? As long as you name a viable, trustworthy beneficiary and explain the necessary tax reporting, your death benefit will be passed along tax-free.

What is a death benefit or Survivor Benefit?

Under an insurance contract, a death benefit or survivor benefit is guaranteed to be paid to the listed beneficiary, so long as premiums are satisfied while the insured or annuitant is alive.

Do you have to pay taxes on money received as a beneficiary?

Beneficiaries generally don't have to pay income tax on money or other property they inherit, with the common exception of money withdrawn from an inherited retirement account (IRA or 401(k) plan). The good news for people who inherit money or other property is that they usually don't have to pay income tax on it.

Are death benefits reportable?

Accordingly, death benefits are “reportable death benefits” under § 6050Y(d)(4), and are subject to the reporting requirements of § 6050Y(c), only if the death benefits are paid by reason of the death of the insured under a life insurance contract transferred after December 31, 2017, in a reportable policy sale.

Do I have to pay taxes on a death benefit annuity?

The proceeds from an annuity death benefit are taxable when they are received by the beneficiary. In the case where the recipient is a surviving spouse, he or she can initiate certain measures to defer the payment or taxes on the amount received.

How are death benefits reported?

The death benefit payment is taxable to the beneficiary in the year IMRF issues the check. If you receive a death benefit payment from IMRF, you would report this payment on the pension line of IRS Form 1040 or 1040A. On the 2002 form this is line 16 on IRS Form 1040 and line 12 on IRS Form 1040A.

Who claims the death benefit on income tax?

A death benefit is income of either the estate or the beneficiary who receives it. Up to $10,000 of the total of all death benefits paid (other than CPP or QPP death benefits) is not taxable. If the beneficiary received the death benefit, see line 13000 in the Federal Income Tax and Benefit Guide.

Is a one time death benefit taxable?

Death Benefit Only Plans Payments are still taxed as ordinary income.

Do you have to report inheritance money to IRS?

Inheritances are not considered income for federal tax purposes, whether you inherit cash, investments or property. However, any subsequent earnings on the inherited assets are taxable, unless it comes from a tax-free source.

Is an inherited annuity considered income?

Annuities are taxed as ordinary income when inherited. The proceeds of an inheritance are taxable. If a beneficiary opts to receive the money all at once, he or she must pay taxes immediately. This is only if you take a lump sum.

What is the death benefit exclusion?

Death benefit exclusion. If you are the beneficiary of a deceased employee (or former employee) who died before August 21, 1996, you may qualify for a death benefit exclusion of up to $5,000. The beneficiary of a deceased employee who died after August 20, 1996, won't qualify for the death benefit exclusion.

Is 1099 R death benefit taxable?

When a taxpayer receives a distribution from an inherited IRA, they should receive from the financial instruction a 1099-R, with a Distribution Code of '4' in Box 7. This gross distribution is usually fully taxable to the beneficiary/taxpayer unless the deceased owner had made non-deductible contributions to the IRA.

Are death benefits from Social Security taxable?

REVENUE ACT OF 1936 Lump sum payments made under section 203 and 204 (b), Title II of the Social Security Act, (49 Stat.,620) to a deceased employee's estate are not subject to Federal income tax and should not be included in the income tax return filed on behalf of the decedent.

Is death lump-sum taxable?

If a death benefit lump sum is not paid within 2 years of when we could first reasonably have been expected to know of the member's death, it may be liable for tax.

What is a Death Benefit?

A death benefit is the purpose of your life insurance policy—when you, the policyholder, pass away, a predetermined amount of money, known as the death benefit, is passed on to your beneficiaries. For final expense, this death benefit will be anywhere from $2,000 to $50,000.

What Does the Final Expense Death Benefit Look Like?

How can you designate your death benefit to be used? Well, you have a few options.

Why Death Benefits Are Not Taxable

With all of this in mind, why are death benefits non-taxable? Well, for the beneficiary, it’s not really income for their own use. You will not see the payout, because it’s only issued once the policyholder (you) passes away.

You Should Still Report On It

Just because life insurance payouts are non-taxable does not mean that you can avoid reporting it. The IRS explains that you should report it under topic number 403, a section designated to taxable, nontaxable, and excludable interest.

Naming a Viable Beneficiary Matters

Be sure, however, to name a beneficiary that will be able to file the death benefit as nontaxable. Minors will have to be placed into a trust to receive the funds, which may be subject to taxation.

Bottom Line?

As long as you name a viable, trustworthy beneficiary and explain the necessary tax reporting, your death benefit will be passed along tax-free. If you are the beneficiary, make sure to discuss these details with the final expense policyholder who named you.

Call Final Expense Direct Today

You and your loved ones financial security is made easy with Final Expense Direct. We will walk you through the insurance process and make sure everything is in proper order. To learn more, give us a call today at 1-877-674-0236.

What happens if you pay death benefits in excess of the stated amount?

When a life insurance company pays death benefits in excess of the stated amount, as you receive these extra dollars, they are taxed as income. Excess benefits typically result from interest earned on your premiums paid during the life of the policy.

What is non-taxable death benefit?

If the policy states that there is no "refund provision" or a stipulated time period guarantee, the non-taxable portion is the amount of death benefit divided by the beneficiary's life expectancy. This equation sounds more complicated than it is mathematically. However, if you are the beneficiary of one of these policies, consult with a tax professional before making your own calculations to avoid tax issues.

What is accelerated death benefit?

Accelerated death benefits are sometimes paid before the insured dies. These amounts, per contract, may be paid when the insured is terminally or chronically ill. These benefits are usually not included in taxable income. According to the IRS, however, this exclusion does not apply for amounts paid to persons or entities, other than the insured, if the person or entity is "a director, officer or employee of the insured" or has a financial interest in the insured's business. You must file IRS Form 8853 with your tax return to claim this exclusion from taxable income.

Is a life insurance policy taxable?

Stated Death Benefit. Life insurance policies with a fixed or stated death benefit that's paid to the beneficiary generate no taxable income. There is an exception, however. If your spouse's employer is the policyholder for your spouse, whether you or the employer is the beneficiary, proceeds above the premiums paid are taxable income to ...

Is a lump sum taxable income?

Whether you receive a lump sum or periodic payments, as long as the amount does not exceed the death benefit specified in the policy, the proceeds are not taxable income. However, should you receive more than the stated death benefit, the additional funds are considered interest and treated as income for tax purposes.

Does the IRS exclusion apply to a director, officer or employee of the insured?

According to the IRS, however, this exclusion does not apply for amounts paid to persons or entities, other than the insured, if the person or entity is "a director, officer or employee of the insured" or has a financial interest in the insured's business.

Is annuity income taxable?

1. Is Annuity Inheritance Taxable? 2. Are Death Benefits From a Company Retirement Plan Taxable? 3. Taxation of Company-Provided Life Insurance. In most, but not all cases, life insurance death benefits are not taxable income. Whether you receive a lump sum or periodic payments, as long as the amount does not exceed the death benefit specified in ...

What is death benefit?

A death benefit is a payment to a beneficiary. The money could come from different types of investments such as stocks, bonds and real estate, or from annuities, life insurance or retirement accounts (e.g., and individual retirement account (IRA), Roth IRA, 401 (k), etc.).

What are the limitations of death benefits?

Every death benefit has its own limitations, such as taxes and creditor protection. Depending on where the money comes from, the restrictions of the death benefit may vary. For instance, death benefits from a life insurance policy are typically paid as a single tax-free lump sum.

What happens if a person dies and leaves behind a mortgage?

If a loved one dies and leaves behind a mortgage to pay, you could use a death benefit to pay off all of, or a portion of, the mortgage. This could help your family remain in the home or limit the debt that's owed before you sell the property. Pay off other existing debt: In conjunction with a mortgage, other household debt may exist ...

Do you have to report interest earned on a death benefit?

You will , however, need to report any interest earned on the proceeds. The proceeds will be paid to those named on the beneficiary form, so this information should be updated regularly as needed. Here are some of the most common types of death benefits and how they're taxed.

Can you use a death benefit to set up an annuity?

Set up an income stream: If you depended on your deceased loved one's income, a death benefit may be used to set up a stream of income through an annuity . This could be a helpful option if family members relied on the deceased person's income to pay for household expenses, such as a mortgage, car loans or credit card debt.

Can you use a death benefit to pay off debt?

Using a death benefit to help pay off debt may be the best option for you . Set up a college fund: After necessary expenses are covered, establishing a college fund for your child (or children) might also be a priority. A death benefit can help fund a 529 college savings plan for you, your child or another family member.

Is annuity income taxable?

In general, the interest earned, which is the difference between the initial amount deposited and the value at death, is taxable at the regular income tax rates and receives no preferential treatment.

What is death benefit?

A death benefit is a sum of money paid out to the beneficiary or beneficiaries of a life insurance policy, as long as the insured died while the policy was in effect. The death benefit is the primary purpose of buying life insurance coverage; it’s what your premium payments cover throughout the life of your policy. Ads by Money.

Who pays out death benefits?

Death benefits are paid out to the beneficiaries you named on your policy. Your life insurance beneficiaries can be one or more persons, a trust that is managed by a trustee, a charity or your estate. You can set up primary beneficiaries and contingent beneficiaries. If you die, your primary beneficiaries are the first in succession to receive ...

What happens if a life insurance policy is lapsed?

A lapsed policy. For a life insurance policy to pay out, the policy must be in force, meaning the policyholder was actively making payments to it. If they neglected to make payments and the grace period expired, the policy could lapse, and the death benefit claim could be denied.

What happens if you have a $1 million policy?

If you have a $1 million policy with $500 in the cash value, your beneficiaries would only receive $1 million upon your death. To get the permanent life policy to pay out both the cash value and the face amount, you could add an optional insurance rider that would increase your premiums further.

How does life insurance work?

How do death benefits work? Life insurance pays out a tax-free death benefit if your policy is active when you die. There are several different types of life insurance policies, but the main categories are term life insurance — the more affordable option — and permanent life insurance.

How long does it take to get a death benefit from life insurance?

Life insurance companies typically take up to a month to review a claim before paying out the death benefit. They may request further documentation.

How long does term life insurance last?

Term Life Insurance. Term life insurance policies are in force for a set period or term, which typically range in length from 10 to 30 years. If the insured dies within the policy term, the insurer pays out a death benefit equal to the policy’s face value.

How to determine taxability of benefits?

The taxability of benefits must be determined using the income of the person entitled to receive the benefits. If you and your child both receive benefits, you should calculate the taxability of your benefits separately from the taxability of your child's benefits. The amount of income tax that your child must pay on that part ...

How to find out if a child is taxable?

To find out whether any of the child's benefits may be taxable, compare the base amount for the child’s filing status with the total of: All of the child's other income, including tax-exempt interest. If the child is single, the base amount for the child's filing status is $25,000.

Is a child's Social Security payment taxable?

If the total of (1) one half of the child's social security benefits and (2) all the child's other income is greater than the base amount that applies to the child's filing status, part of the child's social security benefits may be taxable.

What is death benefit?

Death Benefits. A death benefit is a sum of money paid to one or more beneficiaries when the owner of the death benefit dies. Do not confuse death benefits with the wealth already existing in an account. Rather, death benefits are life insurance payouts on top of the assets accumulated in the decedent’s account.

How long do variable annuities pay out?

Annuities accept contributions up to a certain date and then start paying out assets for a set number of years or until the death of the annuity owner. Most variable annuities come with a death benefit that pays beneficiaries upon the death of the annuitant (who need not be the owner). It is important to separate the payments ...

What happens after a respectful mourning period?

Following a respectful mourning period, beneficiaries will have to make some decisions and file some paperwork to help the decedent’s plans reach fruition. One area that requires special attention is the tax consequences of receiving a death benefit. Most of the time the tax obligations of an inheritance are simple and clear, ...

Why are variable annuities considered variable?

They are "variable" because their returns aren’t guaranteed and depend on the performance of the annuities' investments.

Can a 401(k) be used for life insurance?

Qualified Retirement Accounts. Certain retirement accounts such as 401 (k)s (but not IRAs) can hold life insurance policies with death benefits that pay beneficiaries when the account owner dies. Each year, the account owner must pay income tax on the insurance premiums attributed to pure life insurance protection, ...

Do insurance policies pay taxes on death benefits?

Insurance Policies. In just about all cases, the death benefits paid by insurance policies are free from income tax. However, tax may be due on any interest earned by the death benefit. This situation occurs when the payout of death benefits is delayed.

Can you get death benefits from an annuity?

Death benefits are tied to life insurance policies, retirement plans and annuities. Death benefits can be paid out as lump sums either immediately or at some future date, or they might be paid out in installments over time, as is the case with annuities.

How many Social Security payments can a survivor receive?

If so, the survivor will only receive one payment, and this payment will be the higher of the two between your benefit and his or hers. Also, the survivor’s benefit is based on the age of the survivor. If a spouse receives your monthly Social Security payment, he or she can receive 100% of the amount at full retirement age.

How much is a survivor's Social Security?

This is a one-time payment, and the amount is currently $255.

Can you pass on Social Security to your family?

Many financial retirement plans, including individual retirement accounts, can be passed on to loved ones, and if you and your family rely on your Social Security income for financial stability, it’s important to understand what you can and cannot pass on.

Can a disabled child receive Medicare after death?

Regardless of the situation, a child who is seeking to receive your death benefit must be unmarried. Once again, Medicare benefits can not be passed on after death.

What Is A Death Benefit?

Understanding Death Benefits

- Individuals insured under a life insurance policy, pension, or other annuity that carries a death benefit, enter into a contract with an insurer at the time of application. Under the contract, a death or survivor benefit is guaranteed to be paid to the listed beneficiary, so long as premiums are paid while the insured or annuitant is alive. Beneficiaries have the option to receive death benefit pro…

Requirements For Payout of Death Benefits

- The process of receiving a death benefit from a life insurance policy, pension, or annuity is straightforward. Beneficiaries first need to know which life insurance company holds the deceased's policy or annuity. There is no national insurance database or other central location that houses policy information. Instead, it is the responsibility of each insured to share policy or …

Changes to Retirement Plan Death Benefits

- In 2019, the U.S. Congress passed the SECURE Act, which made changes to retirement plans, including the death benefits from inheriting an IRA.3 The SECURE Act eliminated the so-called stretch provision for beneficiaries who inherit an IRA. In the past, an IRA beneficiary could stretch out the required minimum distributionsfrom the account over their lifetime. Stretching out the di…