6 Ways to Increase Your Social Security Benefits

- Delay Claiming Social Security Benefits. The simplest way to increase your monthly payments is to delay claiming Social Security benefits. ...

- Work for at Least 35 Years. The Social Security Administration uses your 35 highest-earning years to calculate your primary insurance amount (PIA), which is the monthly benefit amount you ...

- Collect Spousal Benefits. Collecting spousal benefits, based upon your spouse’s work record, is another way to beef up your Social Security benefits.

- Apply for Social Security Survivor Benefits. You may also be able to increase your monthly retirement paycheck using Social Security survivor benefits.

- Avoid the Social Security Tax. Social Security benefits may be subject to federal income tax. How much goes to Uncle Sam depends on a somewhat complicated formula.

- Fix an Early Social Security Benefits Mistake. You can also boost your Social Security payments by correcting any previous errors. ...

- Work for at least 35 years.

- Earn more.

- Work until your full retirement age.

- Delay claiming until age 70.

- Claim spousal payments.

- Include family.

- Don't earn too much in retirement.

- Minimize Social Security taxes.

How can you maximize your Social Security benefits?

Use these 6 strategies to increase your household's lifetime benefits

- Don’t Take the SSA’s Advice at Face Value. Going straight to the source seems like a great way to get accurate information about the best time to file for ...

- Withdraw Your Social Security Application. Here’s one opportunity to reverse a claiming decision you regret. ...

- Suspend Your Social Security Benefits. ...

- Maximize Your Household Benefits. ...

How can I get more money SSA?

You may qualify for these benefits if you meet the following criteria:

- You are a U.S. ...

- You're a resident of one of the 50 states, Washington, D.C., or the Northern Mariana Islands.

- You're not absent from the U.S. ...

- You're not confined to an institution at the government's expense.

- You've applied for other cash benefits you may be eligible for, like Social Security retirement benefits and pensions.

- You have limited income.

How much can I earn while on social security?

- Be aware that we are talking about Social Security income limits for retirement benefits, not disability or SSI.

- The earnings limit on Social Security is not the same as income taxes on Social Security. ...

- The earnings limit does not apply if you file for benefits at your full retirement age or beyond. ...

- The earnings limit is an individual limit. ...

How can I get more Social Security benefits?

According to the Social Security Administration, you may qualify for spousal benefits if:

- Your spouse is already collecting retirement benefits.

- You have been married for at least a year.

- You are at least 62 years old (unless you are caring for a child who is under 16 or disabled).

How can I increase my Social Security?

Below are the nine ways to help boost Social Security benefits.Work for 35 Years. ... Wait Until at Least Full Retirement Age. ... Sign Up for Spousal Benefits. ... Receive a Dependent Benefit. ... Monitor Your Earnings. ... Avoid a Tax-Bracket Bump. ... Apply for Survivor Benefits. ... Check for Mistakes.More items...

Can I get money added to my Social Security check?

Last Updated: September 9, 2021 If you, or a family member, receive Social Security or Supplemental Security Income (SSI), certain life changes could entitle you to an increase in your benefit amount.

Is it better to take Social Security at 62 or 67?

The short answer is yes. Retirees who begin collecting Social Security at 62 instead of at the full retirement age (67 for those born in 1960 or later) can expect their monthly benefits to be 30% lower. So, delaying claiming until 67 will result in a larger monthly check.

How do I know if I have 40 credits for Social Security?

Earn 40 credits to become fully insured In 2022, the amount needed to earn one credit is $1,510 . You can work all year to earn four credits, or you can earn enough for all four in a much shorter length of time. If you earn four credits a year, then you will earn 40 credits after 10 years of work.

What does 40 credits mean for Social Security?

The Social Security Administration (SSA) defines “enough work” as earning 40 Social Security credits. More specifically, in 2022, an individual receives one credit for each $1,510 in income, and they can earn a maximum of four credits per year. So, 40 credits are roughly equal to 10 years of work.

Can I buy Social Security credits?

You can't buy Social Security credits, the income-based building blocks of benefit eligibility. You can't borrow them or transfer them from someone else's record. The only way to earn your credits is by working and paying Social Security taxes. In 2022, you earn one credit for each $1,510 in income from “covered” work.

How much money can you have in the bank on Social Security retirement?

$2,000You can have up to $2,000 in cash or in the bank and still qualify for, or collect, SSI (Supplemental Security Income).

What is the average Social Security check at age 62?

According to payout statistics from the Social Security Administration in June 2020, the average Social Security benefit at age 62 is $1,130.16 a month, or $13,561.92 a year.

How much will I get from Social Security if I make $30000?

0:362:31How much your Social Security benefits will be if you make $30,000 ...YouTubeStart of suggested clipEnd of suggested clipYou get 32 percent of your earnings between 996. Dollars and six thousand and two dollars whichMoreYou get 32 percent of your earnings between 996. Dollars and six thousand and two dollars which comes out to just under 500 bucks.

Is Social Security based on the last 5 years of work?

A: Your Social Security payment is based on your best 35 years of work. And, whether we like it or not, if you don't have 35 years of work, the Social Security Administration (SSA) still uses 35 years and posts zeros for the missing years, says Andy Landis, author of Social Security: The Inside Story, 2016 Edition.

What is the lowest Social Security payment?

DEFINITION: The special minimum benefit is a special minimum primary insurance amount ( PIA ) enacted in 1972 to provide adequate benefits to long-term low earners. The first full special minimum PIA in 1973 was $170 per month. Beginning in 1979, its value has increased with price growth and is $886 per month in 2020.

How much Social Security will I get if I make $40000?

Those who make $40,000 pay taxes on all of their income into the Social Security system. It takes more than three times that amount to max out your Social Security payroll taxes. The current tax rate is 6.2%, so you can expect to see $2,480 go directly from your paycheck toward Social Security.

How to increase SSA payments?

To increase your SSA payments, aim to build 35 years of work history. Try to have few or no long stretches where you don't earn an income. Find and correct periods of low or no income as early in your career as you're able to increase your average monthly earnings and get the highest amount you can to retire on.

Why was Social Security created?

Social security was created as a safety net for workers and their survivors. Social security provides income that increases with inflation. Even a small increase in your initial benefit will result in a larger payment each year after you retire. Taking certain actions now and later will allow you to increase the amount of Social Security benefits ...

What age does the PIA increase?

It is age 67 for anyone born in 1960 or later. It is reduced by two months for every year before that. The FRA drops no lower than age 65 for those born in or before 1937. For each year after your FRA that you delay taking payments, you will receive an increase in the PIA of 5.5% to 8% per year.

How to get a ballpark figure of future SSA payments?

The best way to get a ballpark figure of your future SSA payments and to see how increases can affect them is to use an online Social Security calculator. For example, the SSA Quick Calculator projects your benefit amount based on your date of birth, your current earnings, and the date you will retire. Plug in a few values to see how your options may impact your payment amount.

What age can you collect survivor benefits?

Most of the time, widows and widowers are eligible for reduced payments at age 60. By waiting until you reach full retirement age to begin survivor benefits, you can get a higher payment each month.

How much is the PIA increase for 1943?

For instance, someone born in 1943 or later gets an 8% annual increase in PIA, which amounts to a payout increase of two-thirds of 1% each month. There is no point in waiting past age 70 to file, as these increases are not given past that point. 4.

How much tax do you pay on SSA?

Under IRS rules, some people will have to pay federal income tax on up to 50% of their benefits. Some may even have to pay 85% tax on their SSA payments if they make a large amount of combined income.

How to increase Social Security check size?

1. Work at Least the Full 35 Years. The Social Security Administration (SSA) calculates your benefit amount based on your lifetime earnings.

How much will Social Security increase if you wait until 70?

If, for example, you are eligible for a primary insurance amount (PIA) of $2,000, or $24,000, at age 66, then by waiting until age 70, your annual benefit would increase to $31,680.

How does the SSA calculate your Social Security benefits?

The SSA calculates your benefit amount based on your earnings, so the more you earn , the higher your benefit amount will be . Some pre-retirees look for ways to increase their income, such as taking on part-time work or generating business income. Others, however, unaware of the impact on benefits, may scale back on their work or semi-retire, which can lower their Social Security income. 2

Why was Social Security not a primary income source?

Rather, its sole purpose was to provide a safety net for people who were unable to accumulate sufficient retirement savings. For the next several decades, the majority of Americans never gave much thought to their Social Security because of shorter lifespans and reliance on guaranteed pensions.

How long do you have to work to get the most Social Security?

Navigating Social Security income can be complicated, but there are strategies to maximize your Social Security benefits. Working for 35 years or more will help ensure you get the most money when your benefit amount is calculated.

Why did the majority of Americans never give much thought to their Social Security?

For the next several decades, the majority of Americans never gave much thought to their Social Security because of shorter lifespans and a reliance on guaranteed pensions.

When did the SECURE Act change retirement accounts?

Changes were made to the rules regarding retirement accounts with the passage of the SECURE Act in 2019 by the U.S. Congress. A few of those changes include the following:

How much will Social Security increase after retirement?

After your full retirement age, payments will increase by about 8 percent for each year you delay claiming Social Security up until age 70. After age 70, there is no additional benefit for waiting to sign up for Social Security.

How is Social Security calculated?

Social Security benefits are calculated based on the 35 years in which you earn the most. If you don't work for at least 35 years, zeros are factored into the calculation, which decreases your payout.

How much do you get from Social Security if you don't work?

Increasing your income by asking for a raise or earning income from a side job will increase the amount you receive from Social Security in retirement. Earnings of up to $132,900 in 2019 are used to calculate your retirement ...

How long do you have to work to get Social Security?

Try these strategies to maximize your payments: Work for at least 35 years. Social Security benefits are calculated based on the 35 years in which you earn the most.

How to check if your Social Security is paid?

Create a My Social Security account and download your Social Security statement annually to check that your earnings history and Social Security taxes paid have been recorded correctly by the Social Security Administration. Make sure you are getting credit for the taxes you're paying into the system.

Can a spouse inherit a deceased spouse's Social Security?

When one member of a married couples dies, the surviving spouse can inherit the deceased spouse’s benefit payment if it’s more than his or her current benefit. Retirees can boost the amount the surviving spouse will receive by delaying claiming Social Security. Make sure your work counts.

How to boost Social Security benefits?

Retirees can boost their Social Security with a few key strategies. Wait to retire until full retirement age (FRA). Delay applying until age 70 and you’ll get your maximum amount. If you work while getting benefits, make sure you don’t run into the earned-income limits that will reduce your benefits.

How to start collecting Social Security?

Wait until at least full retirement age to start collecting. Collect spousal benefits. Receive dependent benefits. Keep track of your earnings. Watch out for tax-bracket creep if you’re still working. Apply for survivor benefits. Check Social Security statement for mistakes. Stop collecting benefits temporarily.

How old do you have to be to get spousal benefits?

If you’re at least 62 years old and have a child in your care, you may be eligible to receive benefits through your spouse. The spousal benefit can be as much as 50% of the amount of the partner’s benefit, depending on when the partner retires. 7 . Even divorcees are eligible.

What is the maximum retirement benefit for 2021?

As your benefit is based on your highest-earning years, the more you earn, the higher your benefit. There are limits, though. The maximum benefits for 2021 are $2,324 for those retiring at age 62, $3,113 for those retiring at the full retirement age of 66, and $3,895 for those retiring at age 70. 3. 2.

How often do you get a Social Security statement?

You get a Social Security statement every year. 13 Do not assume it is accurate. Check the numbers and report any errors to the Social Security Administration. Remember, your benefits are based on the average of your 35 highest-earning years. A miscalculation for even one or two of those years could impact your benefit for the rest of your life.

How much Social Security do you get if you are retired but still have dependents?

If you are retired but still have dependents under age 19, they are entitled to up to 50% of your benefit . This dependent benefit doesn’t decrease the amount of Social Security benefits that a parent can receive. They are added to what the family receives. 8

What is the maximum amount you can earn on Social Security in 2021?

For 2021, the limit on earned income is $18,960 for recipients below full retirement age and $50,520 in the year when you reach full retirement age. Your benefit payment is reduced for the year if you exceed these limits. 10 After that, however, there is no penalty for earned income at any level.

What is a do over for Social Security?

Another option to consider, especially for baby boomers with poor saving habits, is a "do-over" known as Form SSA-521 – officially, the "Request for Withdrawal of Application." If you've regretted your decision to take Social Security benefits early (and 60% of seniors do file for benefits between ages 62 and 64, ensuring they receive a permanent reduction in their monthly payout), Form SSA-521 may allow you the opportunity to undo your filing.

What is the first factor of interest in Social Security?

This first factor of interest is your average earnings history. In other words, the more you earn, the bigger your payout, up to a certain point.

What happens if you file for Social Security incorrectly?

If the SSA has your earnings history incorrect, it could adversely affect what you're paid once you file for benefits – and it's a lot harder to fix those errors after you begin receiving a monthly benefit check .

Why do women get less Social Security?

That's because more women than men choose to stay home and raise their children, as well as provide caregiving services to sick friends and relatives. This adversely affects their income, which reduces their Social Security benefit. But if their higher-earning spouse passes away, they'll have the opportunity to trade their benefit based on their own work history for the survivor benefit based on their deceased spouse's work history, assuming the survivor benefit is higher.

How long do you have to be married to claim spousal benefits?

If you're now divorced from your spouse, but you were married for at least 10 years , and you're still unmarried and of Social Security claiming age (at least 62), you may be able to claim spousal benefits based on your former spouse's earnings history.

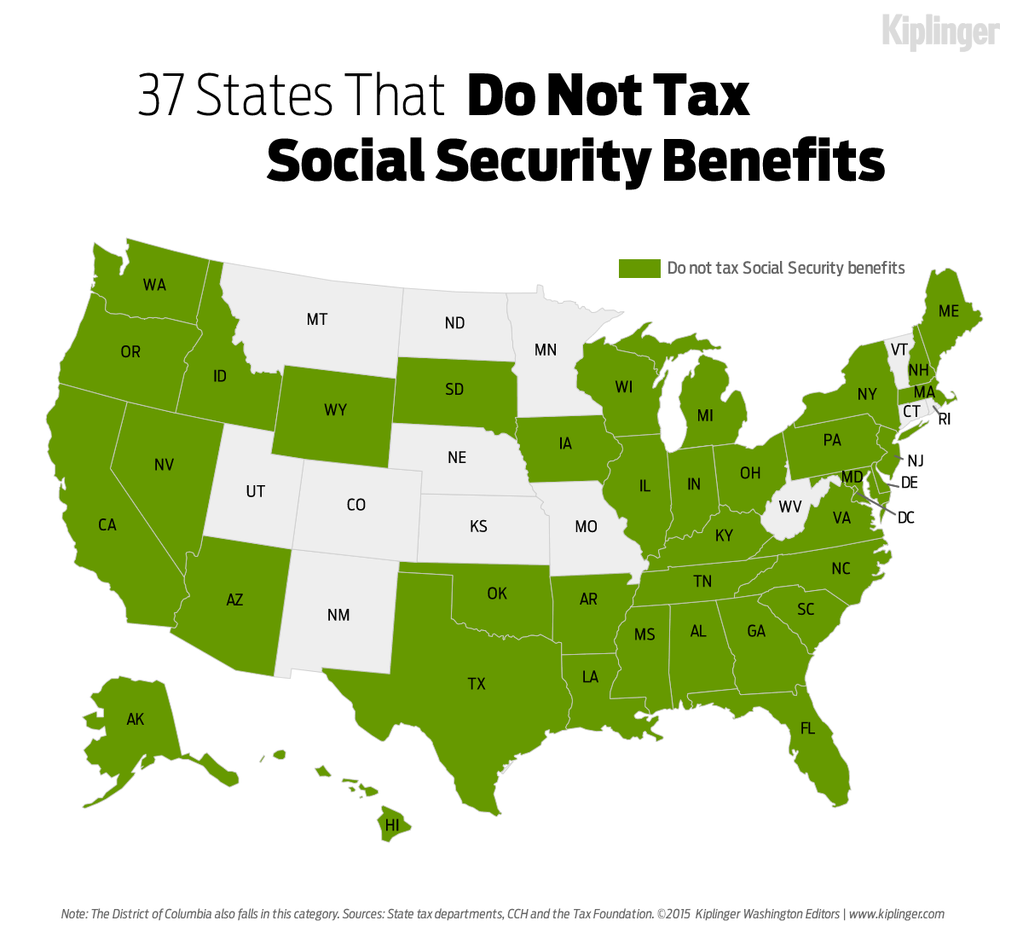

How many states tax Social Security?

However, 13 states also tax Social Security benefits. Should you choose to live in a state that taxes Social Security benefits, you may be required to hand over some of your benefit. If you want to keep as much of your Social Security income as possible, you'll want to pay close attention to where you retire.

What age do you have to be to get a high wage?

Chances are you lacked the skill set necessary to garner a high wage in your teens or early 20s. By your 60s you'll likely have plenty of work experience, which could translate to a higher annual wage even after adjusting for inflation and lift your overall earning average over your 35 highest-earning years.

How to maximize Social Security benefits?

Two other income-boosting strategies give couples a way to maximize their Social Security benefits. A recent paper by the Center for Retirement Research recommends that the spouse who is eligible for lower benefits collect them early, while the higher-earning spouse delays taking benefits until they are worth more. Then, when the primary breadwinner dies, the spouse with the lower benefit will "step up" to a much higher survivor benefit as the smaller retirement payment drops off.

What is the maximum amount you can receive if you delay collecting Social Security?

On the other hand, if you delay collecting benefits, you will receive an 8% credit for every year beyond your normal retirement age until you reach 70, when your maximum benefit will be 132% of what you would have received at age 66. In this example, you would receive about $2,100 a month at 70 -- a $900 difference.

How long does it take to repay Social Security?

That process may take several weeks. Once you repay the benefits, you can reapply for new, higher payments based on your current age.

How much money do you have to pay back if you retire at 62?

If, for example, you received $1,200 a month starting at age 62, plus annual cost-of-living adjustments through age 70, you would have to repay about $130,000. That's a lot of money, but for some people it's worth the price to get an additional $900 a month in retirement. By comparison, it would cost a 70-year-old man about $190,000 to buy an immediate annuity that would provide $900 a month initially, plus annual inflation adjustments and a 100% survivor benefit. That's 46% more expensive than "buying" a lifetime annuity from Social Security.

How much did John Rothenhoefer increase his Social Security?

When John Rothenhoefer, 70, found out that he could increase his Social Security benefits by about $1,000 a month by taking advantage of a do-over strategy, he thought he'd struck gold. As it turns out, he might as well have won a mega lottery.

What is the number to call for Social Security?

But don't expect the claims representatives at your local Social Security office or the employees who answer the agency's toll-free number (800-772-1213) to be familiar with the details. "Our service representatives can go an entire career and never encounter this situation," says Lassiter.

When does a baby get a Social Security check?

When the baby is born, he or she will receive monthly Social Security checks worth up to half of Bill's benefit until the child reaches age 18. Bill plans to stretch those benefits even further by depositing them in a state-sponsored 529 college-savings plan.

How to make the most of Social Security payments?

To make the most of these payments, first determine which spouse will earn a larger benefit. The lower-earning spouse can start claiming Social Security at an earlier age, while the higher-earning spouse’s benefit amount continues to grow. Once the higher-earning spouse reaches 70, the couple can switch to filing against that person’s earnings history.

How much of your Social Security income do you pay in taxes?

You may pay taxes on up to 85% of your Social Security benefits, depending on your tax filing status and income level. And remember: the government considers Social Security benefits, employment earnings and interest from investments as income.

What is the age at which you can claim Social Security?

Income is not the only factor that determines your Social Security benefit. Age is another big one. Normal or full retirement ageis the age at which you can claim the full Social Security retirement benefit you’re eligible for. The Social Security Administrationdetermines your full retirement age based on the year you were born. For most people, the magic number falls somewhere between 65 and 67. When you know your full retirement age, you can make a better-informed decision about when to start claiming Social Security.

What to do if your estimated benefits are not as much as you were hoping for?

If your estimated benefits are not as much as you were hoping for, try earning more money. An income boost will improve the average of your 35-year earnings record, which could give your benefits a much-needed bump too.

What is Survivor's Social Security?

Survivor’s payments are Social Security benefits designed to help replace lost retirement income if your spouse passes away. As a widow or widower, you can elect to receive ongoing benefits beginning at age 60.

How many years do you have to work to get Social Security?

In reality, your payments are based on your earnings from the 35 highest income years. If you have not worked for 35 years, every year you didn’t work will reduce your benefits.

Is it too early to start planning for retirement?

It’s never too early to start planning for retirement. A retirement calculatorcan help you figure out how much you’ll need to retire comfortably. Building a sizable nest egg may enable you to delay Social Security benefits and maximize your monthly payments once you are ready to collect.

How does Social Security work before becoming disabled?

If you worked for a number of years and paid Social Security taxes before becoming disabled, your benefit will be based on your earnings and tax history. The Social Security Administration allows you to set up an account where you can view a personalized estimate of disability benefits. Your Social Security statement will explain what you are eligible for and how much to expect each month.

How does Social Security work?

The Social Security Administration allows you to set up an account where you can view a personalized estimate of disability benefits. Your Social Security statement will explain what you are eligible for and how much to expect each month. By and large, the formula used to calculate your disability benefits is set.

How long do you have to wait to apply for disability?

If your impairment makes it impossible to work and is predicted to last, you can apply for disability benefits right away. You don’t have to wait until a full year has passed to apply. Ask your physician for help filling out forms, communicating the diagnosis and reporting the information.

How many people are disabled on Social Security?

(Getty Images) Approximately 1 in 4, or 61 million, adults in the United States report a disability, according to data from the U.S. Department of Health and Human Services.

Can life changes affect disability?

Life changes could impact your disability eligibility. There may be other ways to receive assistance. Read on to learn how Social Security disability checks are issued and what you can do to increase your overall income when facing a disability. A Guide to Social Security Disability. ]

Can you get disability if you are no longer disabled?

Even if you have been receiving benefits for several years, your eligibility could change if it is determined that you are no longer disabled. “Benefits are not guaranteed for life,” says Jerry Zivic, a recently retired attorney in Sarasota, Florida, who practiced Social Security Disability law for more than 30 years.

How to find out if you qualify for Social Security?

To find out if you, or a family member, might be eligible for a benefit based on another person’s work, or a higher benefit based on your own work, see the information about benefits on the Social Security website. You can also use the Benefit Eligibility Screening Tool (BEST) to find out if you could get benefits that Social Security administers. Based on your answers to questions, this tool will list benefits for which you might be eligible and tell you more information about how to qualify and apply.

Why do we have a second Social Security representative?

We also want to make sure you receive accurate and courteous service. That is why we have a second Social Security representative monitor some telephone calls.

How old do you have to be to get unemployment benefits?

If you are at least 62 years old and unmarried, you may be eligible for a benefit based on a former spouse’s work if that marriage lasted 10 years or more.

Can my survivor benefit increase if my spouse dies?

Has your spouse or ex-spouse died? If your spouse or ex-spouse has died, you may be eligible for a higher survivor benefit based on his or her work. The death of an ex-spouse may allow you to be eligible for a higher survivor benefit even ...

Can you get a higher Social Security if your spouse dies?

It's not unusual for a benefit recipient's circumstances to change after they apply or became eligible for benefits. If you, or a family member, receive Social Security or Supplemental Security Income (SSI), certain life changes may affect eligibility for an increase in your federal benefits. For example, if your spouse or ex-spouse dies, you may become eligible for a higher Social Security benefit.