Are there tax benefits associated with life insurance?

There are two important tax advantages associated with life insurance. The first tax advantage is that death benefits are generally not taxable as income for income tax purposes for a person named as the beneficiary. The second tax advantage is that for cash value plans, there is generally no tax on the increase in the cash value as it grows over time.

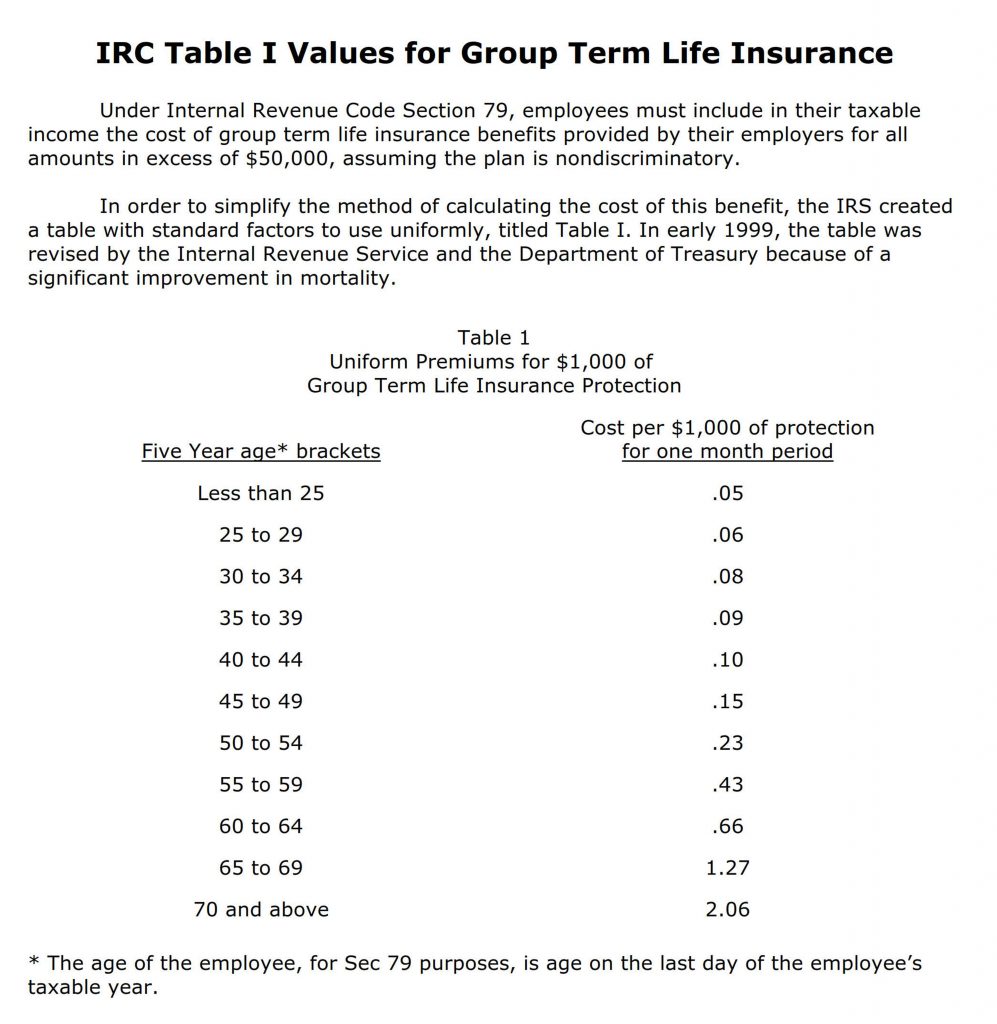

What are the tax benefits of offering life insurance?

What are the tax benefits of offering life insurance? Companies who meet the non-discrimination requirements for life insurance can generally exclude the cost of up to $50,000 for group-term life insurance from the wages of an insured employee. The company can also exclude the same amount from the employee's wages when calculating the employee ...

Is life insurance ever subject to income taxation?

Is life insurance subject to income taxes? Usually, the answer is no. The proceeds of the death benefit are usually considered to be income tax free to the beneficiary because the policy owner had already paid taxes on the premium. Where the taxation would change would be where a tax deduction was taken on the premium.

Does life insurance count as taxable income?

Life insurance income that can be taxable if the contract is a modified endowment contract or the life insurance cash values are annuitized. Universal life insurance policies issued after June 21, 1988 with gain in the contract that is governed under TAMRA could cause withdrawals to be taxed during the first 15 years of the policy.

Is life insurance payout considered earned income?

Regarding your question: Is life insurance payout taxable income, no, the IRS does not consider life insurance payouts taxable income. However, life insurance payout taxable interest issues might arise if you earn interest on the payouts after the relative dies.

Do insurance payouts count as taxable income?

Money you receive as part of an insurance claim or settlement is typically not taxed. The IRS only levies taxes on income, which is money or payment received that results in you having more wealth than you did before.

How much tax do you pay on life insurance payout?

Is a life insurance payout taxable? One of the perks of a life insurance policy is that the death benefit is typically tax-free. Beneficiaries generally don't have to report the payout as income, making it a tax-free lump sum that they can use freely.

Is a lump sum death benefit taxable?

While some forms of death benefits, such as life insurance payments, are not subject to income tax, the IMRF lump sum death benefit is taxable. Payments from insurance are not subject to income tax because the member paid the premiums on the policy using previously taxed money.

Are Life Insurance Premiums Taxable?

The life insurance premiums you pay are not taxable. They are also not deductible on your tax return.

Do You Pay Inheritance Tax on Life Insurance?

There is no inheritance tax on life insurance. Life insurance death benefits are paid tax-free to your life insurance beneficiaries.

Is There a Penalty for Cashing Out Life Insurance?

If you surrender a cash value life insurance policy, the only “penalty” is that you may have to pay a surrender fee. The life insurance company wil...

When are life insurance proceeds tax-free?

Generally, your beneficiaries can dodge taxes in these situations.

Are life insurance premiums tax-deductible?

Unfortunately premiums aren’t tax-free, even if you’re paying for an individual policy. You also can’t use a Flexible Spending Account (FSA) or Hea...

When is life insurance taxable?

With so much riding on your life insurance, speak with a licensed accountant if you’re still unsure about the tax implications of your specific pol...

What is the unlimited marital deduction?

The unlimited marital deduction is a provision in the federal Estate and Gift Tax Law that allows you to pass any amount of assets to your spouse d...

What happens if you get $250,000 in life insurance?

So if your $250,000 life insurance benefit gains $25,000 in interest between time of your death and payout, your beneficiaries would likely owe taxes on the accrued $25,000. To avoid this, beneficiaries should choose to receive the lump sum.

How much money do you owe if you cancel a life insurance policy?

If you cancel your policy, you’ll likely owe taxes on the $30,000 you’ve earned.

What happens if you cancel your life insurance policy?

If you decide to cancel your life insurance policy before it matures, you’re eligible to gain access to your accrued cash value minus any surrender fees. This is called a “life insurance surrender,” and as long as your settlement amount is less than the total you paid in premiums, your surrender payout is tax-free.

How long before death can you transfer a life insurance policy?

Just keep in mind that if you transfer the policy less than three years before your death, it might still be subject to the estate tax. Note that the IRS offers an unlimited marital deduction that allows you to transfer unlimited assets to your spouse, free of any estate or gift taxes.

How much estate tax is required for 2020?

If your estate is valued at $11.58 million – the IRS threshold for 2020 – or more, it will be subject to federal estate tax. This applies to life insurance payouts, too.

Is life insurance taxable?

One of the main selling points of life insurance is that the proceeds are typically not taxable. There are a few situations where beneficiaries will have to pay tax — and they usually apply to permanent policies or policyholders with large estates.

Can you receive life insurance after you die?

After you die, your life insurance beneficiaries often can choose to receive your policy’s death benefit as a lump sum or in installments over time. If they choose installments, the policy’s insurer holds the death benefit, which may accrue interest, depending on the account it’s held in.

What happens to cash value life insurance when the beneficiary dies?

When the policy holder dies, the full cash value goes back to the insurance company ...

What happens if you don't pay back your life insurance?

In a way, you’re cannibalizing your life insurance by eating away at the provision you’ve established for your family.

How many people are involved in a life insurance policy?

When Three People Are Involved. When you think about it, there are really only three roles in a life insurance policy: the owner of the policy, the insured person and the beneficiary. If there are only two people in this scenario, the policy is not taxable. For example, if the owner is the insured person, there’s no tax!

How is taxable estate calculated?

Your “taxable estate” is calculated by taking this estate value and subtracting any unpaid loans from the cash value account. If this figure is over $11.4 million, the estate will have to pay taxes. Remember to check with your state laws too, because some have their own estate tax set up.

What is estate tax?

Estate Tax – Basically, the federal government and some states combine all the assets of the deceased (property, investments, annuities and life insurance), subtract all that is owed (loans, medical bills and credit cards), and then they tax the final number. This tax is paid from the estate itself, not the individuals involved.

When is a death benefit in force with no taxes due?

Here are two ways to look at trusts and taxes: If you set up the irrevocable trust from the beginning as the owner and the beneficiary of the life insurance policy, then the death benefit is in force with no taxes due from day one.

Is death benefit taxable income?

For example, if the owner is the insured person, there’s no tax! But if a father (the owner) buys a life insurance policy on his son (the insured), then names his daughter-in-law as the beneficiary, the death benefit is taxable income for the daughter-in-law.

How to keep life insurance out of your estate?

One way to keep your life insurance death benefit out of your estate is to transfer ownership to someone else before you die. But be mindful of the three-year rule, which states a policy is still part of your estate if a transfer of ownership occurs within three years of your death.

What happens when you surrender a life insurance policy?

When you surrender a permanent life insurance policy, you’re essentially canceling the coverage, and the insurer pays out the policy’s cash value, minus any surrender fees. The portion of the cash value that exceeds the policy basis is taxable.

What is the federal estate tax exemption limit?

The federal estate tax exemption limit is $11.58 million, which means if your estate’s total taxable value is greater than this amount, the IRS levies an estate tax. The bottom line is that if you know your estate won’t exceed $11.58 million, you don’t need to worry about this tax. Plus, proceeds left to your spouse are typically exempt from estate tax, even if they exceed the federal limit.

Is life insurance paid to spouse taxable?

Plus, proceeds left to your spouse are typically exempt from estate tax, even if they exceed the federal limit. However, if you own your life insurance policy when you die, the IRS includes the payout in your estate, regardless of whether you name a beneficiary. This could push your estate’s total taxable value over the federal exemption limit ...

Does life insurance pay lump sum?

Instead of a lump sum payout, the life insurance beneficiary might receive the death benefit in installments. If this happens, the insurer typically holds the principal amount in an interest-bearing account and issues a percentage of the death benefit over a set number of years.

Is death benefit tax free?

One of the perks of a life insurance policy is that the death benefit is typically tax-free. Beneficiaries generally don’t have to report the payout as income, making it a tax-free lump sum that they can use freely. That being said, there are exceptions.

Is life insurance taxable?

For the most part, life insurance proceeds are not taxable. That’s good news if you’re the beneficiary of your great-aunt’s million-dollar policy. But don’t start spending the money in your head just yet. Some situations can lead to taxation, particularly if you earn interest on the proceeds.

How Life Insurance Payouts Work

When the insured dies, the policy beneficiary must file a death claim to the insurance company and submit a certified copy of the death certificate. After a review process is completed, the policy payout goes to the named beneficiary (ies).

Understanding Taxation on Life Insurance Proceeds

Consult with a licensed life insurance agent or tax professional when buying the policy to ensure your policy will produce the tax benefits you want.

Life Insurance Death Benefits Are NOT Taxable

Let’s get straight to the point: No, your life insurance policy’s death benefit is not subject to taxes. While that money can be used in ways that trigger a taxable event, the payout itself is not taxable.

How the Money is Used Matters

Depending on how your loved ones use the money from a life insurance death benefit, there can indeed be taxes involved. They just won’t be triggered from the initial payout.

How the Money is Received Matters

Generally, life insurance proceeds are paid out to your loved ones in a lump sum. In some cases, though, you or your beneficiaries can choose an annuity (also known as a life income payout), which will instead spread payments out over a determined period of time.

Certain Policy Benefits Can Trigger Taxes

If your life insurance policy builds a cash value over time — as is the case with many whole and universal life policies — you, as the primary insured, can generally borrow from this balance as needed.

Surrendering Your Policy is Taxable

Another benefit to the cash value of permanent life insurance policies is that if you decide to cancel your coverage down the line, you’ll get at least a portion of that money back thanks to the policy’s accumulated cash value .

Bottom Line

Buying life insurance coverage is an excellent way to provide your loved ones with a financial safety net in case something were to happen to you. While there are some caveats, life insurance benefits are generally not subject to taxes, meaning that your beneficiaries can keep every dollar of your policy’s proceeds, when they need it most.

How to contact a life insurance agent about estate taxes?

Connect with a licensed life insurance agent online or by calling 1-855-303-4640. ----------.

What is the difference between permanent and term life insurance?

A permanent (or cash value) life insurance plan provides coverage for the insured person's entire life. They also accumulate cash value over time. Term life insurance. Term life plans provide coverage for a set agreed-upon length of time , called a term. They do not accrue cash value like permanent policies.

Does life insurance have to be reported to the IRS?

An exception is if you receive interest on a benefit — any interest that has been earned must be reported to the IRS and is potentially subject to income tax. There are two main categories of life insurance policies: A permanent (or cash value) life insurance plan provides coverage for the insured person's entire life.

Do death benefits fall under estate tax?

Because the insurance policy increases the estate’s value, the benefits may fall under the estate tax if your estate is large enough.

Is life insurance subject to income tax?

Life Insurance Benefits Not Subject to Income Tax. Here’s the good news. For the most part, the federal government doesn’t tax the proceeds benefits from a life insurance policy.

Is life insurance taxable?

If you’re shopping for a life insurance policy, you may be wondering if life insurance is taxable. Income to the beneficiary is one of the main purposes of a life insurance plan. Typically, the death benefit of a life insurance policy is not subject to income tax. However, some exceptions may apply.

How to remove life insurance from taxable estate?

Using Life Insurance Trusts to Avoid Taxation. A second way to remove life insurance proceeds from your taxable estate is to create an irrevocable life insurance trust (ILIT). To complete an ownership transfer, you cannot be the trustee of the trust and you may not retain any rights to revoke the trust.

What happens when you transfer a life insurance policy?

In transferring the policy, the original owner must forfeit any legal rights to change beneficiaries, borrow against the policy, surrender, or cancel the policy, or select beneficiary payment options. Furthermore, the original owner must not pay the premiums to keep the policy in force.

How to transfer insurance policy?

Here are a few guidelines to remember when considering an ownership transfer: 1 Choose a competent adult/entity to be the new owner (it may be the policy beneficiary), then call your insurance company for the proper assignment, or transfer of ownership, forms. 2 New owners must pay the premiums on the policy. However, you can gift up to $15,000 per person in 2020, so the recipient could use some of this gift to pay premiums. 4 3 You will give up all rights to make changes to this policy in the future. However, if a child, family member, or friend is named the new owner, changes can be made by the new owner at your request. 4 Because ownership transfer is an irrevocable event, beware of divorce situations when planning to name the new owner. 5 Obtain written confirmation from your insurance company as proof of the ownership change.

What happens if you get a death benefit of $500,000?

If the death benefit is $500,000, for example, but it earns 10% interest for one year before being paid out, the beneficiary will owe taxes on the $50,000 growth. According to the IRS, if the life insurance policy was transferred to you for cash or other assets, the amount that you exclude as gross income when you file taxes is limited to ...

What happens when you name an estate as a beneficiary?

However, when you name the estate as your beneficiary, you take away the contractual advantage of naming a real person and subject the financial product to the probate process. Leaving items to your estate also increases the estate's value, and it could subject your heirs to exceptionally high estate taxes .

Does a life insurance beneficiary have to pay taxes?

Generally speaking, when the beneficiary of a life insurance policy receives the death benefit, this money is not counted as taxable income, and the beneficiary does not have to pay taxes on it. However, a few situations can exist in which the beneficiary is taxed on some or all of a policy's proceeds. If the policyholder elects not ...

Is life insurance income taxable?

Income earned in the form of interest is almost always taxable at some point. Life insurance is no exception. This means when a beneficiary receives life insurance proceeds after a period of interest accumulation rather than immediately upon the policyholder's death, the beneficiary must pay taxes, not on the entire benefit, but on the interest.