Advantages of a 15-Year Mortgage

- Less in Total Interest. A 15-year mortgage costs less in the long run since the total interest payments are less than a 30-year mortgage.

- Lower Interest Rate. Since short-term loans are less risky and cheaper for banks to fund than long-term loans, a 15-year mortgage typically comes with a lower interest rate.

- Fannie Mae. If your mortgage is purchased by one of the government-sponsored companies, like Fannie Mae, you will likely end up paying less in fees for a 15-year loan.

- Forced Savings. Since the monthly payment is higher for a 15-year mortgage, financial planners consider it a type of forced savings.

What are the advantages of a 15 year mortgage?

Pros of 15-Year Mortgages

- Shorter Debt Horizon. No one likes debts hanging around their necks. ...

- Build Equity Faster. Sure, building equity in your home feels nice. ...

- Lower Interest Rate. Mortgage lenders charge lower interest rates for shorter-term loans. ...

- Lower Total Interest Paid. The lower interest rate aside, borrowers still pay more in interest for longer-term loans. ...

Why a 15 year mortgage is a smart move?

When interest rates are rising, the conventional wisdom says that refinancing your mortgage is less appealing. But for some homeowners, a 15-year refinance mortgage could be a smart financial move. Shorter mortgage terms help you increase your home equity faster.

Is a 15 year mortgage better than a 30 year?

While a 30-year mortgage can make your monthly payments more affordable, a 15-year mortgage generally costs less in the long run. Most homebuyers choose a 30-year fixed-rate mortgage, but a 15-year mortgage can be a good choice for some. A 30-year mortgage can make your monthly payments more affordable.

How much house can I afford 15 year mortgage?

While you may have heard of using the 28/36 rule to calculate affordability, the correct DTI ratio that lenders will use to assess how much house you can afford is 36/43. This ratio says that your monthly mortgage costs (which includes property taxes and homeowners insurance) should be no more than 36% of your gross monthly income, and your total monthly debt (including your anticipated monthly mortgage payment and other debts such as car or student loan payments) should be no more than 43% ...

Is it better to get a 30-year mortgage and pay it off in 15 years?

If your aim is to pay off the mortgage sooner and you can afford higher monthly payments, a 15-year loan might be a better choice. The lower monthly payment of a 30-year loan, on the other hand, may allow you to buy more house or free up funds for other financial goals.

Why is it better to take out a 15-year mortgage instead of a 30?

The advantages of a 15-year mortgage The biggest benefit is that instead of making a mortgage payment every month for 30 years, you'll have the full amount paid off and be done in half the time. Plus, because you're paying down your mortgage more rapidly, a 15-year mortgage builds equity quicker.

Which is an advantage of taking a 15-year mortgage?

Build equity faster A 15-year fixed-rate mortgage, with its lower interest rate and higher payment amount, builds home equity faster because you pay down the principal balance quicker.

What are the pros and cons of getting a 15-year mortgage versus a 30-year mortgage?

15-year mortgage pros and cons15-Year Mortgage Pros15-Year Mortgage ConsLower interest rates than 30-year fixed-rate mortgagesHigher monthly paymentsLower total cost of interest over the life of the loanLess cash left over for investing, emergency funds, and other expenses1 more row•Aug 17, 2021

How can I pay off a 15-year mortgage in 5 years?

Five ways to pay off your mortgage earlyRefinance to a shorter term. ... Make extra principal payments. ... Make one extra mortgage payment per year (consider bi-weekly payments) ... Recast your mortgage instead of refinancing. ... Reduce your balance with a lump-sum payment.

What happens if I pay an extra $400 a month on my mortgage?

The additional amount will reduce the principal on your mortgage, as well as the total amount of interest you will pay, and the number of payments. The extra payments will allow you to pay off your remaining loan balance 3 years earlier.

What are disadvantages of a 15-year mortgage?

Disadvantages of a 15-Year MortgageFirst-time homebuyers may lack the finances to qualify.Higher locked-in monthly payments leave little extra cash flow for other purchases.Higher debt-to-income ratio prevents qualification for other large loans.

How do I pay my house off in half the time?

How to Pay Off Your Mortgage FasterMake biweekly payments.Budget for an extra payment each year.Send extra money for the principal each month.Recast your mortgage.Refinance your mortgage.Select a flexible-term mortgage.Consider an adjustable-rate mortgage.

Do you pay less interest on a 15-year mortgage?

The interest rate is lower on a 15-year mortgage, and because the term is half as long, you'll pay a lot less interest over the life of the loan. Of course, that means your payment will be higher, too, than with a 30-year mortgage.

How can I lower my mortgage interest rate without refinancing?

There is one way you can get a lower mortgage interest rate without refinancing, however....Your lender may adjust your loan by:Extending your loan term.Reducing your principal balance.Lowering your mortgage rate.

Is a 10 year mortgage worth it?

If you're approaching retirement with a steady income, the 10-year fixed-rate mortgage may be a good choice. This may be ideal for those looking to close out their mortgages sooner rather than later. However, it's vital that anyone considering this loan be prepared for retirement with a healthy retirement fund.

Which loan term is the best financially?

A 15-year loan is best if …You can comfortably afford a higher monthly mortgage payment. Your monthly principal and interest payments will be significantly higher on a 15-year loan. ... You want to build equity more quickly. ... You're buying a house well within your means. ... You plan to stay in your home short term.

What is a 15 year mortgage?

A 15-year mortgage is the dream home loan for buyers who can afford higher monthly payments and want to pay off their mortgage in half the usual time. A 15-year timeline can save thousands or even tens of thousands of dollars in interest. To make a 15-year fixed-rate mortgage work, you’ll need a reliable income and enough money left ...

Why is a 15 year fixed rate mortgage better?

A 15-year fixed-rate mortgage, with its lower interest rate and higher payment amount, builds home equity faster because you pay down the principal balance quicker.

How many times as many 30-year mortgages are written?

Your taxes and insurance costs can change, though. In 2018, lenders wrote nearly 22 times as many 30-year home purchase mortgages as they did those with 15-year terms, according to NerdWallet analysis of Home Mortgage Disclosure Act data.

How long does it take to pay off a 15 year mortgage?

What is a 15-year mortgage? A 15-year mortgage will be paid off completely in 15 years if you make all the payments on schedule. These mortgages typically have a fixed rate, which keeps the principal and interest rate the same for as long as you hold the mortgage. Your taxes and insurance costs can change, though.

What happens if you put 20% down on a mortgage?

This could make it hard to respond to emergencies and other needs. Even if numbers seem doable now, a mortgage is a commitment. Getting out means selling, refinancing or foreclosure.

Does a 15 year mortgage have a lower interest rate?

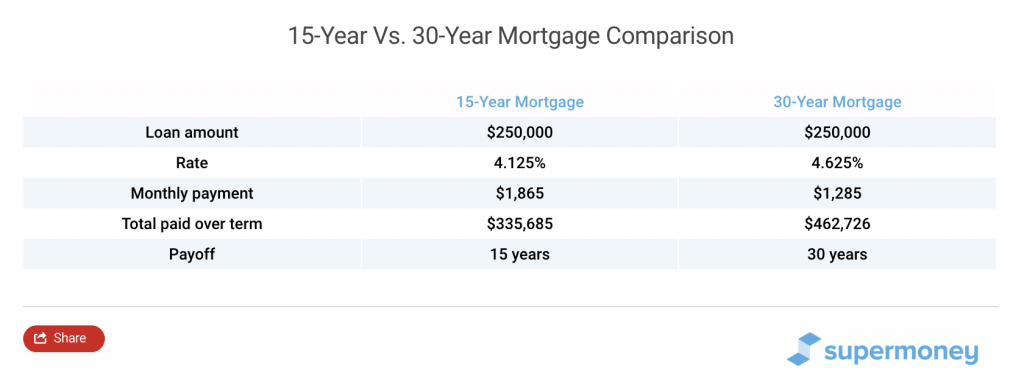

Lenders are exposed to fewer years of risk on a 15-year mortgage, so they charge a lower interest rate. Half as many years of payment also means you pay half as many years of interest. Let’s compare the principal and interest — not including homeowners insurance, property tax or private mortgage insurance — for a $250,000 mortgage ...

1. You spend less on interest

You can save your money on interest in two ways with a 15-year mortgage. One is you can pay off your home loan in half the time, so you are spending less because you’re not carrying a loan for all that extra time.

2. You're debt-free sooner

Generally, mortgage debt is considered a healthy debt, and credit card debt is considered problematic.

3. Pay off your mortgage prior to retirement

Though it is not compulsory to pay off your home by the time of your retirement yet entering retirement ‘mortgage free’ is a happy and peaceful feeling.

Why do financial planners view a 15 year mortgage as a kind of forced savings plan?

Why do many financial planners view a 15-year mortgage as a kind of forced savings plan? As Investopedia explains, you’re investing in your house by building equity. That equity is an asset that you can draw on if you need to, but it would require deliberate, thoughtful action on your part to do so. Add the fact that property tends to appreciate in value in the long run to the calculation, and it’s clear that your investment in your home could result in a nice financial nest egg.

Is a 15 year mortgage better than a 30 year mortgage?

Some borrowers see that a 15-year mortgage will have a higher monthly mortgage payment than a comparable 30-year mortgage and immediately cross this form of financing off their list of possibilities ( source ). Don’t make the same mistake. While the higher monthly payment may be a bit of a turnoff, borrowers who look beyond it to explore the benefits of a 15-year mortgage may be surprised by how advantageous these loans can be. Although it may seem counterintuitive, agreeing to a home loan with higher monthly payments can actually save you money in the long run and help you amass wealth faster. How does it work?

How much would you pay if you paid off a mortgage in 15 years?

If you took the same terms but paid off the mortgage in 15 years, you'd pay $1,471 a month. Now, granted, your interest rate would likely be lower, but even if your interest rate dropped to 2.92 percent, you'd still pay $1,373 a month.

Is 15 year mortgage interest lower than 30 year?

It isn't just that you've shaved off 15 years' worth of interest ( though, yes, that's a plus), but the rates are usually lower for a 15-year mortgage than a 30-year mortgage. Typically, interest rates are 0.75 to 1 percent lower, says Casey Fleming, a San Francisco-based mortgage advisor and author of the book, ...

Is a 15 year mortgage higher than a 30 year mortgage?

Con: The monthly payments for a 15-year mortgage are higher than a 30-year. For instance, if you took out a $200,000 mortgage at a 3.92 percent interest rate for 30 years, your monthly payments would be $946 (without factoring in taxes and other costs). If you took the same terms but paid off the mortgage in 15 years, you'd pay $1,471 a month.

Is a 15 year mortgage a double bonus?

So a 15-year mortgage yields a double bonus, so to speak," Fleming says. But if you're thinking, "I am going to get a 15-year mortgage and become rich with savings," well, not so fast. There are some drawbacks. Con: The monthly payments for a 15-year mortgage are higher than a 30-year.

What is the average interest rate for a 15 year mortgage?

So, make sure to shop around for the best rate and analyze every offer you receive. Currently, 15-year mortgages average 2.52 percent , versus 3.18 percent for a 30-year.

Is a 15 year mortgage better than a 30 year mortgage?

Yes, 15-year mortgages tend to have lower interest rates than their 30-year counterparts, but because you have to pay off the balance in half the time, you wind up laying out more each month while you’re making those payments. “That’s usually where everyone’s stress is.

Can you refinance a 30 year loan into a 15 year loan?

Interest rates are still low enough that some mortgage holders who refinance old 30-year loans into new 15-year ones can actually keep their monthly payments pretty similar. “People are able to shorten the amortization period,” Lazerson said, and the result is savings you don’t have to think about.

1. Lower Interest Rates

As a 15-year mortgage is a shorter-term loan, it is less risky for the lenders and the chances of a borrower defaulting on a loan is correlated to the duration of the payback period. Therefore, most lenders offer comparatively lower interest rates on 15-year mortgage programs.

2. Saves Money on Interest

When you choose a 15-year mortgage program to finance your home, not only are you paying a lower interest rate, but more of your payment is going towards principal (which goes to actually paying off the loan) versus more going to paying interest (which goes to paying the lender).

3. Less Fees

Another advantage of opting for a 15-year mortgage loan is that you need to pay less fees. The government sponsored enterprises (GSE’s) charge lower fees for loan level price adjustments on 15-year mortgages than they do for 30-year mortgages. These fees apply to all borrowers who have a lower credit score or make a small down payment, or both.

Summing It Up

Based on the above, borrowers who can afford a higher monthly payment may want to consider opting for a 15 year mortgage over a 30 year mortgage.

How much interest do you pay back on a 15 year mortgage?

You're paying back a loan of $250,000 that charges a 4.5 percent interest rate. If you added $200 a month to your monthly payment, you could reduce the payback on a 15-year mortgage to around 12.5 years. This would also save you nearly $13,000 in interest costs.

What is the average mortgage rate for a 30 year loan?

Mortgage rates just keep heading lower, defying expectations. Currently, the average rate is 3.56 percent for a fixed-rate 30-year loan. That’s nearly a half a percentage point lower than the rate just a year ago, according to Freddie Mac. Meanwhile, home values have been heading higher.

What credit score do I need to refinance a mortgage?

If refinancing interests you, Ellen Steinfeld, managing director of consumer lending at TIAA Direct online bank says you would be in line for "attractive rates" if you have at least 20 percent equity and a FICO credit score of at least 700. FICO scores range from 300-850. According to mortgage data firm Ellie Mae, the average FICO credit score for borrowers who refinanced for a conventional mortgage recently was 732.

Does taking out a mortgage add up to closing costs?

Their total debt payments (including the mortgage) added up no more than 38 percent of their income on average. Keep in mind that taking out a new mortgage will come with closing costs. You can choose to pay upfront, or accept a slightly higher interest rate if you don’t want to use cash to cover your closing costs.

Is it a good time to refinance a 15 year mortgage?

With rates so low, it's also a good time to consider refinancing into a 15-year mortgage instead of a 30-year mortgage. Typically, homeowners prefer 30-year mortgages. Halving the payback period often means making a much higher monthly payment.

Can I refinance my mortgage if I have 15 years?

If you have 15 years or less remaining on your existing mortgage you may not want to refinance, says Germi Cloud, a financial advisor in Huntsville, Ala. “You’ve paid most of the loan’s interest costs in the first 15 years, so you don’t want to start paying more interest now.”

Why do people get 15 year mortgages?

Some borrowers opt for the 15 year mortgage because it saves them a significant amount of money in the long term. The market today is filled with several types of mortgage products. The 15 year mortgage has its own set of advantages and disadvantages in comparison to the 30-year. While both the products share similarities, ...

Why do I need to refinance a 15 year mortgage?

A homebuyer can save significant money over the length of the loan with a 15-year mortgage because the interest paid is less than in a 30-year mortgage. Refinancing into a 15-year mortgage when you are halfway through your 30-year mortgage, may lower your interest payments while still paying off the loan in the expected amount of time.

What is the monthly payment for a 30 year loan?

Whereas a 30-year loan would result in a $1,194 monthly payment that is under the $1,500 limit approved by the lender, the 30-year loan might allow the borrower to buy a larger home or take on a bigger mortgage.

How much does a 30 year mortgage cost?

So a 30-year mortgage for a $300,000 home would cost $1,432 per month, which too is under the $1,500 maximum and allows you to take on a larger loan by getting a bigger home or a better location.

When do you have to pay PMI?

Lenders require PMI when you put a down payment that is smaller than 20% of the home’s value. PMI protects the lender in case you default on the payments. It is charged as a monthly fee added to the mortgage payment, and it ceases once you pay off 20% of your mortgage.

Is a 15 year mortgage less than a 30 year mortgage?

Since the total interest payments of a 15-year mortgage are less than a 30-year mortgage it would cost less in the long run. The cost of a mortgage is calculated on an annual interest rate and as you’re borrowing the money for half the term, the total interest paid will also be lower than what you’d pay over 30 years.

Does Fannie Mae charge for 15 year mortgage?

If the mortgage is purchased by Fannie Mae, one of the government-sponsored companies, you will end up paying less in fees for a 15-year loan. Fannie Mae and the other government-backed enterprises charge loan-level price adjustments for 30-year-mortgages.