Following are the Benefits of having Life Insurance

- Life Risk Cover. Life insurance provides you with a high life risk cover that keeps you and your family protected in case of an unfortunate event.

- Death Benefit. Investing in life insurance gives you and your family a secure future. ...

- Return on Investment. Life insurance schemes yield better when compared to other investment alternatives. Most of the life insurance schemes offer bonuses that no other investment scheme can offer.

- Tax Benefits. Section 80C of the Income Tax Act is an effective way for the salaried person to reduce tax liability.

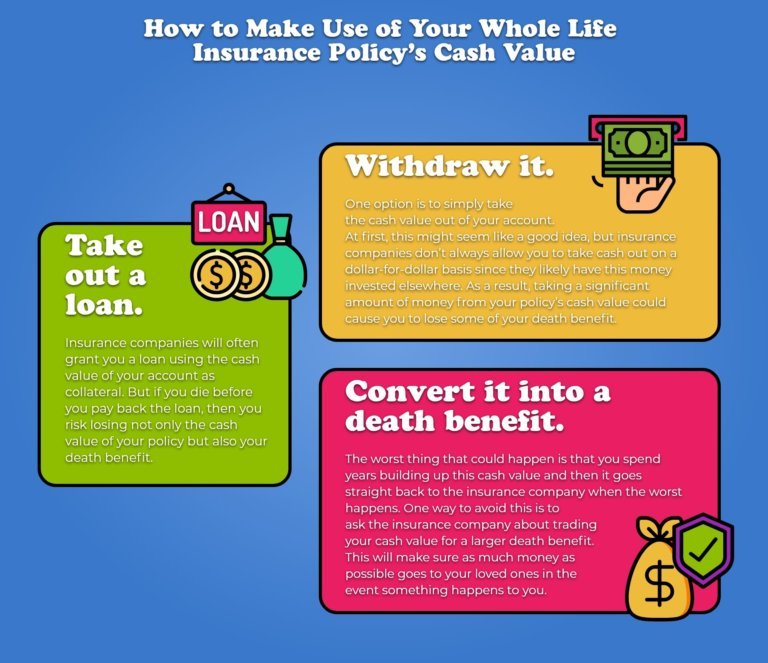

- Loan Options. Life insurance provides you the advantage of taking a policy loan in case you are in desperate need of money.

- Life Stage Planning. Life insurance aids you in life stage planning where you can plan your life’s financial goals as per your convenience.

- Assured Income Benefits. Your family stays secured due to the assured income they receive on regular intervals. ...

- Riders. Riders are the additional benefits that can be bought and added to a basic insurance policy. These options allow you to increase your insurance coverage.

What are the pros and cons of life insurance?

Life insurance isn’t usually top of mind for Canadian retirees focused on generating income from their investment portfolios. Yet certain types of life insurance can play an important role in the lives of older Canadians, especially when it comes to ...

What are the benefits of having life insurance?

- The biggest benefit of life insurance is financial security for your loved ones.

- A death benefit can be used to pay for anything and doesn't have stipulations on spending.

- Certain life insurance policy add-ons (riders) can increase the benefits of your coverage.

Why should I buy life insurance?

- Supplement retirement income

- Fund a child or grandchild’s education

- Pay off a mortgage

- Protect existing assets

- Establish an emergency fund

What is life insurance, and how does it work?

Life insurance is one of the best ways you can ensure your family is taken care of financially when you pass, either by providing enough funds to pay off a mortgage, or by giving them the money they need to live in comfort without your income.

What are the three benefits of life insurance?

The many benefits of having life insuranceIncome replacement for years of lost salary.Paying off your home mortgage.Paying off other debts, such as car loans, credit cards, and student loans.Providing funds for your kids' college education.Helping with other obligations, such as care for aging parents.

What are the pros and cons of life insurance?

The main advantage of owning a life insurance policy: If you die, your beneficiaries. receive a payout called a death benefit that replaces any income you provided while you were alive. The biggest disadvantage: You have to pay monthly or annual premiums for this benefit.

What are the five benefits of insurance?

5 reasons why insurance mattersProtection for you and your family. ... Reduce stress during difficult times. ... To enjoy financial security. ... Peace of mind. ... A legacy to leave behind.

What are the four benefits of insurance?

Benefits of InsuranceCover against Uncertainties. It is one of the most prominent and crucial benefits of insurance. ... Cash Flow Management. The uncertainty of paying for the losses incurred out of pocket has a significant impact on cash flow management. ... Investment Opportunities.

Why life insurance is a waste of money?

Basic life insurance policies are designed to provide replacement funds that can approximately match what the policy owner was making or a percentage of it. A life insurance policy on someone with no earnings or someone with no dependent beneficiaries can be a waste of money.

Can you pull money out of your life insurance?

Withdrawing Money From a Life Insurance Policy Generally, you can withdraw money from the policy on a tax-free basis, but only up to the amount you've already paid in premiums. Anything beyond the amount you've already paid in premiums typically is taxable. Withdrawing some of the money will keep your policy intact.

How do life policies work?

Life insurance is a contract between you and an insurance company. Essentially, in exchange for your premium payments, the insurance company will pay a lump sum known as a death benefit to your beneficiaries after your death. Your beneficiaries can use the money for whatever purpose they choose.

What are the 3 main types of insurance?

Then we examine in greater detail the three most important types of insurance: property, liability, and life.

What is the most important insurance to have?

Health insurance is arguably the most important type of insurance. A 2016 Kaiser Family Foundation/New York Times survey found that one in five people with medical bills filed for bankruptcy. With a stat like this, investing in health insurance can help you prevent a significant financial hardship.

Who would not need life insurance?

If an individual has accumulated enough wealth to take care of their family upon their passing, then life insurance may not be necessary. Couples that have built a life together should have life insurance in case one of them passes away so that the other can maintain the same quality of life.

What are the benefits of life insurance?

The many benefits of having life insurance. All life insurance can give you financial confidence that your family will have financial stability in your absence. But generally, the more life insurance you have, the more benefits it will provide to your family when needed. For example, some people receive a nominal amount ...

Why is life insurance so expensive?

Life insurance generally gets more expensive with age, so many seniors get policies with just enough coverage to provide for funeral expenses to avoid burdening their family. Life insurance can also be used for estate planning strategies, where it can be a tax-advantaged way to leave assets to heirs.

Why do life insurance companies give younger customers lower rates?

Life insurance companies generally give younger customers lower rates for reasons that are easy to understand: They tend to have a longer life expectancy. They are less likely to have been diagnosed with a serious disease. They are likely to pay premiums over a longer number of years.

How to get life insurance at work?

Your employer may provide life insurance as a benefit, or you may opt to pay for additional life insurance through payroll deductions.

What happens to a whole life policy when you die?

A whole life policy is permanent life insurance that last your entire life.

What are the benefits of a home mortgage?

Paying off your home mortgage. Paying off other debts, such as car loans, credit cards, and student loans. Providing funds for your kids’ college education. Helping with other obligations, such as care for aging parents. Beyond your coverage amount, different kinds of policies can provide other benefits as well: ...

When do whole life policies pay dividends?

Some whole life polices do not have cash values in the first two years of the policy and don’t pay a dividend until the policy’s third year. Talk to your financial representative and refer to your individual whole life policy illustration for more information.

What are the benefits of life insurance?

5 Top Benefits of Life Insurance. Life insurance provides a number of useful benefits. Among them: 1. Life Insurance Payouts Are Tax-Free. If you have a life insurance policy and die while your coverage is in effect, your beneficiaries will receive a lump sum death benefit. Life insurance payouts aren’t considered income for tax purposes, ...

What can you use the cash value of a life insurance policy for?

If you purchase a whole, universal, or variable life insurance policy, it can accumulate cash value in addition to providing death benefits . As the cash value builds up over time, you can use it to cover expenses, such as buying a car or making a down payment on a home.

Why don't people have life insurance in 2021?

Kat Tretina. Updated Feb 8, 2021. Life insurance can be essential for protecting your family financially in case of a tragedy, but many people go without it. In fact, nearly half of American adults do not have life insurance, according to a recent survey. 1 One reason is that people assume life insurance is too expensive.

Is life insurance more expensive than a 401(k)?

However, a life insurance policy should not replace traditional retirement accounts like a 401 (k) or an IRA. What's more, cash value life insurance is considerably more expensive than term life insurance, which has no savings component but simply a death benefit.

Is life insurance affordable?

And, life insurance might be more affordable than you think. If you decide to get coverage, check out Investopedia's list of the best life insurance companies of 2021 .

Does life insurance cover funeral expenses?

Life Insurance Can Cover Final Expenses. The national median cost of a funeral that included a viewing and a burial was $7,640 as of 2019. 4 Because many Americans do not have enough savings to cover even a $400 emergency expense, having to pay for a funeral can be a substantial financial burden.

Is life insurance considered income?

Life insurance payouts aren’t considered income for tax purposes , and your beneficiaries don’t have to report the money when they file their tax returns. 3 . 2. Your Dependents Won’t Have to Worry About Living Expenses. Many experts recommend having life insurance that's equal to seven to 10 times your annual income.

Why should I invest in life insurance?

Investing in life insurance gives you and your family a secure future. In case of any untoward happening to the insured, the insurer pays up the entire amount i.e. the sum assured plus the bonus to the bereaved family. Life insurance also safeguards the interest of people who have diminishing incomes with advancing age, people who meet with accidents or for retired people. There are numerous policies available and you can choose the policy that will best suit your requirements.

How much does term insurance premium increase?

Your premium is decided on age at which you buy the policy and remains same, throughout your life. Premiums can increase between 4-8% each year after your Birthday. Your policy application could be rejected or premiums increase by 50-100%, if you develop a lifestyle disease. See how age affects Term Insurance Premiums.

What is life stage planning?

Life Stage Planning. Life insurance aids you in life stage planning where you can plan your life’s financial goals as per your convenience. It helps you plan for your life stage needs. Life Insurance not only provides for financial support in the event of untimely death but also acts as a long term investment.

Is life insurance a necessity?

Verdict. It goes without saying that life Insurance is an absolute necessity. It is a risk minimization and protection tool that must be purchased without any thought or choice. After all it is the question of a life that supports a considerable number of people.

Is life insurance better than other investment options?

Life insurance schemes yield better when compared to other investment alternatives. Most of the life insurance schemes offer bonuses that no other investment scheme can offer. The money invested in life insurance is safe and covers risks.

Does PolicyBazaar endorse insurance?

Disclaimer: Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by an insurer.

1. Tax Benefits

The payments made out to the insurance company as part of a premium payment plan qualify for tax deductions as per the section 80 C of Income Tax Act and as per the policy in case of the death of the insured client then as per the policy clause the family gets a compensation and these returns are exempted from tax and thus remain tax free.

2. Security of Family

A financially responsible adult would look to not only provide for those dependent on him in the present but would plan to secure their future in case of his untimely passing, a insurance policy is a best way to move forward with that plan.

3. Protect Their Home

In case that the insured client has taken out a home loan to build a home for their family and protect their future and then in case of their sad demise the family wouldn’t be able to pay this loan and would be under debt and thus in order to clear that debt would have to sell their home which was the legacy of the client and security of their future here insurance policy could help pay that debt and ensure that the client’s family have a roof over their head and ensure them and financial security..

4. Coverage For Chronic And Terminal Insurance

Many insurance services let the client add an additional rider to their life insurance policy which helps enhance and accommodate the coverage for the expense of your terminal illness and that can be settled with the help of death benefits available to the insured client as per the policy norms.

5. Retirement Savings Benefits

Most life insurance policies offer an additional maturity benefit along with the usual death benefit and this maturity benefit pays out the premiums paid along with interest and additional bonuses upon the maturity of the policy though they come up with a high premium but ultimately the pros outweigh the costs of such policies.

Can you support your family without life insurance?

You can support your family. Did you know that four in 10 households without life insurance would have difficulty paying for living expenses if the their primary household earners passed away? Having an adequate life insurance policy gives you and your loved ones peace of mind knowing your family has the financial means to pay for daily living expenses and future costs, like college tuition for your children.

Is life insurance tax free?

Life insurance benefits are tax-free. Life insurance payouts are not considered income for tax purposes, so your family will get the money they need without a tax burden.

What is the advantage of life insurance?

The main advantage of owning a life insurance policy is that if you die, your beneficiaries receive a payout called a death benefit that replaces any income you provided while you were alive. The disadvantage is that you have to pay monthly or annual premiums for this benefit.

What is life insurance?

Life insurance is the exchange of a relatively small payment each month — a premium — for a very large amount of money if you die — a death benefit. A high enough death benefit covers living expenses, such as a mortgage, and your kids’ college tuition. It can also provide a financial cushion for unforeseen expenses.

How much does life insurance cost?

Depending on how much coverage you need and your age when you apply, you may be paying as little as $20 per month in life insurance premiums for a term life insurance policy. You can lower your coverage amount and term length to get even lower premiums that fit into your budget.

How does term life insurance expire?

Term life insurance expires by the time you have fewer expenses. If you buy life insurance coverage early enough, you could save hundreds of dollars each year compared to buying coverage later in life. → Use our life insurance calculator ...

Why do life insurance companies charge more for coverage?

Your premiums are determined by your medical profile, family medical history, and age, so life insurance companies will charge you more for coverage if your profile flags anything that could potentially increase your risk of dying early.

How long does it take to get free life insurance quotes?

It’s easier than ever to apply for life insurance. Policygenius makes it easy to compare life insurance prices online. In just about 10 minutes, you can get free quotes from many different life insurance companies, and choose the one that fits your needs from there.

Why is whole life insurance so expensive?

Whole life insurance is much more expensive because it lasts your whole life; you’re guaranteed to die while it’s active as long as you’ve been paying your premiums. But most people don’t need as much life insurance after they retire, when they don’t have any dependents, their home is paid for, and they don’t have any outstanding loans. That means the extra years you spend paying whole life insurance premiums past retirement age don’t return as much bang for your buck.

What is the benefit of adding a long term care policy to your life insurance?

Long-term care benefits. Adding a long-term care benefit to your permanent life policy lets you tap into the death benefit to cover long-term care expenses that your health insurance doesn’t cover . The death benefit is typically reduced by the amount of the long-term benefit that you use.

What is term life insurance?

Term life insurance covers you for a set amount of time, or term. It provides funds to your beneficiary (or beneficiaries) if you pass away during that time. Living benefit options for term life include: Accelerated death benefits. This living benefit pays out a portion of your term life policy if you ever face a terminal illness.

What is a withdrawal from a permanent life insurance policy?

A withdrawal lets you access a portion of the cash value of your permanent life policy . You won’t owe any taxes on this withdrawal if the amount you withdraw is less than or equal to your premium payments. ...

What is a surrender policy?

Policy surrender. A policy surrender is when you cancel your permanent life policy to access the cash value portion as a one-time lump sum. The insurer will give you that amount, less any outstanding loans and/or unpaid premiums. Long-term care benefits. Adding a long-term care benefit to your permanent life policy lets you tap into ...

Does life insurance cover you after you die?

While life insurance generally benefits your loved ones after you pass away, it can also benefit them (and you) before that time comes through something known as living benefits.

Can you be charged interest on accelerated death benefit?

You may be charged interest on the portion of the accelerated death benefit that you use.

Do you have to have a credit check to take out a loan against a permanent life policy?

You’ll be charged interest if you take out a loan against your permanent life policy, but it’s usually lower than the interest charged by other lenders. You also won’t have to undergo a credit check or abide by a long list of restrictions.

What is life insurance?

Life insurance is there to protect your family financially after you’re gone. But what if you need the money sooner? Some life insurance policies allow you to accelerate the death benefit or access your cash value early, an option called “living benefits insurance.”. If you’re wondering “what is living benefits insurance,” here’s how term life ...

What is a living benefit rider?

A living benefit rider, which allows someone to get the payout from accelerated death benefits, can offer extra peace of mind, whether or not you end up needing it, just like regular term life policies.

What is accelerated death benefit?

A living benefits rider allows you to access a portion of your payout while you’re still alive if you’ve been diagnosed with a serious condition.

What is Fidelity Life?

At Fidelity Life, our goal is to make life insurance simple, affordable, and understandable for everyday families. This content is intended for educational purposes only. Each post is carefully fact-checked, reviewed and updated regularly to ensure the information is as relevant as possible.

Is a living benefits rider a good choice?

Consider your health history: Does Alzheimer’s, cancer, or another serious illness run in your family? If so, a living benefits rider may be a good choice.

Is cash value more expensive than term life insurance?

You can borrow against it or use it as collateral if you need extra money for expenses. While whole life policies are more expensive than term life insurance, they can provide permanent protection and extra support if the worst happens.

Can you add a rider to a life insurance policy?

You can add a rider to an existing policy or a new one, typically for an extra cost. One of the most common riders is a living benefits or terminal illness rider, also known as an accelerated death benefit rider.