What are the advantages of an USDA loan?

- USDA Loan = 1%

- FHA Loan = 1.75%

- VA Loan = 2.15%

- Conventional loans do not have a funding fee

What qualifies for an USDA loan?

Other eligibility requirements include:

- U.S. citizenship (or permanent residency)

- A monthly payment — including principal, interest, insurance and taxes — that’s 29% or less of your monthly income. ...

- Dependable income, typically for a minimum of 24 months

- An acceptable credit history, with no accounts converted to collections within the last 12 months, among other criteria. ...

What are the basic requirements for obtaining an USDA loan?

- Pay stubs for the last 30 days

- W-2s for the last two years

- Bank statements for the last 60 days

- Federal tax returns for the last two years

- Proof of homeowners insurance

- 1099 forms (if you’re self-employed or commissioned)

- Documented dividends, stock earnings and other sources of income

- Proof of bonus income

- Pension statements

What banks offer USDA loan?

- Caliber Home Loans: To get in touch with someone at Caliber Home Loans (either through messaging or on the phone), you have to create an account with the lender first.

- Carrington Mortgage: You'll need a credit score closer to 700 to get a USDA loan with Carrington.

- PNC Bank: You must have at least 3% down for a USDA loan.

What is the downside to a USDA loan?

Cons to the USDA Rural Development Loan Geographic restrictions. Mortgage insurance included (may be financed into loan) Income limits. Single family, owner occupied only - no duplex homes.

What are the advantages of getting a USDA loan?

No Down Payment! The fact that the USDA loan program allows homebuyers to achieve 100% financing, and put $0 towards buying their home is undoubtedly the most significant benefit of using a USDA loan.

Is it worth getting a USDA loan?

A USDA loan is a great option for buyers with moderate or low income. It lets you buy a house with nothing down and low mortgage rates — two huge benefits that only one other loan program (the VA loan) offers. If your home is in an eligible area, it's worth exploring a USDA-guaranteed loan.

What's the difference between a USDA loan and a regular loan?

Conventional loans are available nationwide. USDA loans, on the other hand, are only available in eligible rural areas as determined by the USDA. If you're located in a major metropolitan area, you likely won't be able to get a USDA loan.

Do you pay back USDA loans?

USDA housing repair loans Loans amounts can't be more than $20,000, and borrowers have 20 years to pay the loan back. The interest rate stays at 1% for the life of the loan. The program also makes grants available for the same use for eligible people who are at least 62 years old and can't afford to repay a loan.

What credit score do you need for USDA loan?

640Approved USDA loan lenders typically require a minimum credit score of at least 640 to get a USDA home loan. However, the USDA doesn't have a minimum credit score, so borrowers with scores below 640 may still be eligible for a USDA-backed mortgage.

Does USDA annual fee ever go away?

USDA may assess a late fee to the lender if the annual fee is not paid when due. The applicable upfront guarantee fee and/or annual fee may differ for a purchase and refinance transaction. The annual fee will cease to be collected when 80% loan to value (LTV) is achieved. WAY TO GO!

Is USDA or FHA better?

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements. There are no income limits when you apply for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow.

Do sellers not like USDA loans?

Seller concessions for USDA loans are among the most buyer-friendly out there. Conventional buyers can't tap into that 9 percent cap unless they're putting down 20 percent. USDA's approach to closing costs and concessions is one more reason buyers should give this loan program a closer look.

Is FHA easier to get than USDA?

Lenient credit requirements: You can generally qualify for maximum FHA financing with a credit score of 580 versus a 640 score for a USDA loan. You might also be eligible with a credit score between 500 and 579 if you can make a 10% down payment.

Can USDA loan be used on fixer upper?

A USDA renovation loan allows you to finance 100% of the purchase and 100% of your renovation costs, plus repairs up to the “as-improved” market value. That means you can buy and renovate a fixer-upper with no down payment. So, can you buy a fixer-upper with a USDA loan? Yes.

Do USDA loans have PMI?

So no, USDA loans don't require PMI; only conventional loans have PMI, and only on those loans where the borrower has less than 20% equity in their home. Other loan programs may have their own forms of mortgage insurance. On FHA loans, mortgage insurance is referred to as a mortgage insurance premium (MIP).

How much down payment do you need for a USDA mortgage?

Front and center, the most attractive feature of the USDA mortgage is the no down payment requirement. Most loans will require the borrower to pay between 3% and 20% down at the time of purchase. On a home priced at $225,000, this means the borrower will have to pay between $6,750 and $45,000 upfront, just to get the loan.

What is a rural home loan?

Too many people are under the impression that the term “rural” used to describe the rural housing home loan means a home located well away from a major city. However, that is not really the case.

How much closing cost do you have to pay for a home loan?

The rules state that a seller may choose to pay up to 6% of the home’s asking price in closing costs for the loan. It is not required for the seller to make this concession, but it is allowed. In order for the seller to pay the closing costs, they will need to be detailed in the purchase contract.

How much does a conventional loan cost?

A conventional loan will charge between 0.55% and 2.25% depending on certain factors like credit score, loan-to-value ratio, and debt-to-income ratio. In contrast, the USDA home loan charges a one-time 1% upfront fee which you can include in the loan amount. Also, they charge 0.35% annually for a funding fee.

How much does FHA charge for mortgage insurance?

The funds are used in case the borrower is no longer able or willing to make the house payments and the home is foreclosed. FHA charges 0.85% ( 95 percent or over loan-to-value) of the outstanding loan amount each year for private mortgage insurance. A conventional loan will charge between 0.55% and 2.25% depending on certain factors like credit ...

Is there a limit on the amount of income you can borrow?

However, there is a restriction on the amount of the borrower’s income. The restrictions are based on the number of people that will live in the home once the loan papers are signed. These restrictions vary slightly from county to county and from state to state.

Does USDA limit the size of a mortgage?

One feature that is almost unique to USDA mortgages is the fact that there is no limit on the loan size. As long as the borrowers meet the credit requirements and the income requirements, USDA does not restrict the size of the home loan. However, there is a restriction on the amount of the borrower’s income.

No down payment, No problem

We know that financial hurdles, like down payments, can make home buying seem impossible for many hopeful buyers. That’s why we are proud to offer the U.S. Department of Agriculture’s Rural Housing Loan (USDA loan). A USDA* loan is one of the most powerful mortgage options available to rural and suburban homebuyers.

1. No Down Payment!

The fact that the USDA loan program allows homebuyers to achieve 100% financing, and put $0 towards buying their home is undoubtedly the most significant benefit of using a USDA loan.

2. Lower-Than-Market Interest Rate

Because the U.S. Department of Agriculture insures USDA loans, homebuyers are offered a low, across-the-board interest rate that does not vary based on their credit score or down payment. In comparison, with conventional financing, interest rates are dependent on the market and the borrower’s credit score.

3. Low Monthly Private Mortgage Insurance (PMI)

Private mortgage insurance is required for any loan with less than a 20% down payment, regardless of the loan program, this includes USDA loans.

4. Flexible Credit Guidelines

USDA loans allow some borrowers with blemished or limited credit histories to be eligible for home financing. Those with no credit or non-traditional credit may qualify if they show a willingness to repay their debts with, proof using rent, utilities, cell phone bills, etc.

5. Closing Cost Assistance

Closing costs range between 2% and 5% of the purchase price – another significant expense when buying a house. With a USDA loan, the seller can pay up to 6% of your closing costs, or you can ask that your closing costs be included in your mortgage loan. Closing costs can be financed up to the appraised value of the home.

Who is Eligible for a USDA Loan?

The USDA loan is an amazing option for first-time homebuyers, but repeat homebuyers may qualify as well! Click here for more information on how you can get a USDA loan and eligibility or contact one of our mortgage bankers.

What is the closing cost of a USDA loan?

Costs generally range between 3% and 5% of the purchase price – another big expense when buying a house. With a USDA loan, the seller can pay your closing costs or they can be financed up to the appraised value of the home. Additionally, gift funds can be used to pay closing costs.

Is there a maximum purchase price for USDA loans?

Although borrowers must fall within the USDA income limits to qualify for a loan, there is no maximum purchase price. And, after a review of a borrower’s credit, income and existing debt, lenders determine the amounts based on the borrower’s ability to repay and their debt to income ratios.

Can you finance closing costs with USDA?

Another option for closing costs, is to roll the costs into the loan. Yes, with USDA you can finance your closing costs. The trick to this option is that the house must appraise for more than the asking price and USDA will finance up to 100% of the appraised value.

Who is the USDA backed by?

USDA loans are backed by the U.S. Department of Agriculture and are intended to help people living in low- to moderate-income households put down roots in certain rural and suburban locations.

Is rural development suburban?

It's certainly an option if that's what you're looking for, but many areas that fall under the Rural Development umbrella are actually more suburban than you'd expect. As an example, rural development in northern Indiana covers most areas except Gary, South Bend and Fort Wayne.

Can you borrow 100 percent of the appraised value?

And you can borrow 100 percent of the appraised value. That means you do not have to come up with funds for the down payment, which can be a challenge for many homebuyers. If you think this means you'll be living down a long winding country road with the closest neighbor a mile away, you're mistaken. It's certainly an option if that's ...

What is the USDA loan?

The U.S. Government offers a number of mortgage products that are less restrictive and more affordable than conventional loans. One example is the USDA Rural Development home loan, backed by the U.S. Department of Agriculture. Originally designed to help rural citizens become homeowners, geographic eligibility has significantly expanded over the years. Because the USDA guarantees 90% of each loan in case of borrower default, lenders can extend attractive features to borrowers like 0% down-payment options, low interest rates and minimal insurance costs.

What is USDA financing?

Like the VA and FHA, the USDA allows for renovations and improvements to new and existing properties when the cost is rolled into the purchase or refinance transaction.* The USDA allows for financing of up to 102% of the appraised home value in order to make improvements. Funds can be used for essential household equipment, energy efficiency upgrades, installing or updating utilities, or outfitting the house to accommodate a disability, among other things.

Is a USDA loan reserved for farmers?

A common myth about USDA loans is that they’re reserved for farmers and borrowers who live in the country. Actually, the definition of “rural” applies to roughly 97% of the U.S. land area! Even if the property you want to buy or refinance is located in a city suburb, it may still qualify geographically for a USDA home loan.

What credit score do I need to qualify for USDA?

Many conventional lenders have a minimum score of at least 660, however some may require a credit score as high as 720 in order to qualify.

Do you need a down payment for a USDA loan?

Arguably the best benefit of a USDA loan is that no down payment is required. With 100% financing you can purchase a home sooner. USDA and VA loans are the only government-backed loan options that don’t require a down payment.

Is USDA loan interest lower than other mortgages?

As USDA loans are backed by the United States Department of Agriculture, their corresponding interest rates may be lower than other mortgage options . While rates vary from lender to lender, and can change based on other factors, USDA loans offer competitive rates and savings.

Do USDA loans have PMI?

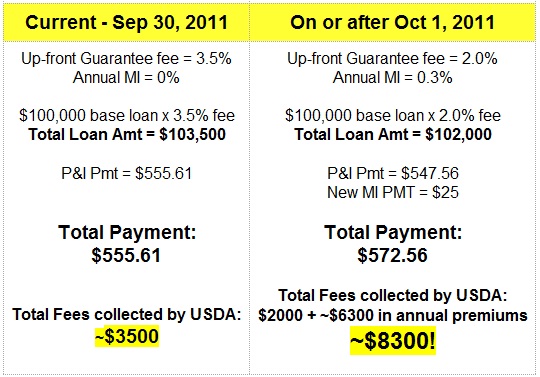

PMI, or private mortgage insurance, is required for conventional loans if less than 20% of the value’s value is put down. USDA loans do not have PMI. However, they have two fees that other loan types do not. An upfront guarantee fee is paid when you close on your USDA loan. This is a 1% fee of the total financed amount. There is also an annual fee that is combined with your monthly mortgage payment. The annual fee is 0.35% of the loan’s current balance. Combined these fees are typically lower than a PMI payment, and the annual fee will decrease as your balance becomes lower.

What is USDA loan?

USDA loans are government-backed mortgages insured by the U.S. Department of Agriculture (USDA). They’re meant to help low- and moderate-income borrowers buy homes in qualifying locations, including rural and suburban areas throughout the country.

Why is USDA mortgage interest so competitive?

Competitive interest rates. Because the USDA mortgage program has the backing of the U.S. government, this reduces the risk for mortgage lenders, allowing them to offer low interest rates — even for borrowers with no down payment. A lower rate means a lower monthly payment and less paid in interest over the long run.

How much down payment is required for USDA mortgage?

Unlike most other mortgage loans, USDA mortgages require zero down payment. This can amount to huge savings up front. An FHA loan, for example, requires at least 3.5% down. On a $200,000 home purchase, that’d be $7,000. Conventional buyers pay slightly less at 3% (still $6,000!).

What are the two types of USDA loans?

There are two types of USDA rural development loans: Guaranteed and Direct. The Direct loans are for very low- and low-income borrowers, and you have to apply directly through the USDA. The USDA Single-Family Guaranteed loans are offered through USDA-approved lenders, and those are what we’ll be referring to in this article.

Is every home eligible for a USDA loan?

Not everyone — or every property — is eligible for a USDA loan, as there are strict income and location requirements. Additionally, USDA loans come with lifetime mortgage insurance premiums (MIP), although USDA’s MIP rates are lower than those for FHA loans.

Does the USDA grant the ability to approve loans?

Longer underwriting times. For loans like FHA and VA, lenders have the authority to review and approve loans entirely on their own. USDA does not grant that ability to lenders. The USDA itself reviews each loan file after the lender approves it.

Can you use a USDA loan on a vacation home?

USDA loans cannot, however, be used on investment properties or vacation homes. Mult-unit properties are not eligible for USDA, even if you plan to live in one unit. If you’re in the market for a 2-4 unit home, consider FHA over USDA.