Key Takeaways

- A death benefit is a payout to the beneficiary of a life insurance policy, annuity, or pension when the insured or annuitant dies.

- Beneficiaries must submit to the insurer proof of death and proof of the deceased's coverage.

- Beneficiaries of life insurance policies receive the death benefit payment free of ordinary income tax.

How to make a death claim in life insurance policy?

Usually, you require the following documents to process a death claim:

- Death certificate

- Original policy documents

- ID proof of the beneficiary

- Age proof of insurer

- Discharge form (executed and witnessed)

- Medical certificate (as proof for cause of death)

- Police FIR (in case of unnatural death)

- Postmortem report (in case of unnatural death)

- Hospital records/certificate (if the deceased died due to an illness)

What does death benefit mean in life insurance?

- The death benefit amount depends on your income and financial needs.

- There is generally no tax applied to the death benefit payout.

- Minor children cannot be direct recipients of the death benefit.

Do you pay taxes on life insurance death benefits?

Typically, beneficiaries on a life insurance policy will not be required to pay income tax when they receive a death benefit, but there are certain exceptions to this rule.

How is my life insurance death benefit calculated?

- A policy owner may temporarily need a higher amount of insurance. ...

- A policy owner may need a death benefit that will continue to increase. ...

- A policy is purchased as part of a savings strategy designed to supplement retirement to rapidly build cash value by over-funding the policy in the early years. ...

How much do you get from life insurance when someone dies?

The beneficiary receives the full amount of the death benefit unless there are multiple beneficiaries. In that case, the policyholder typically specifies how much money each beneficiary will receive. It's also the beneficiary's responsibility to file a claim after the policyholder's death.

Do you get the cash value and the death benefit?

Do beneficiaries get the cash value and the death benefit? Most of the time, no — the cash value can only be used while you, the policyholder, are alive. The cash value remains completely separate from the death benefit, and cannot be accessed by your beneficiaries, even when you die.

How much is a death benefit?

Widow or widower, age 60 — full retirement age — 71½ to 99% of the deceased worker's basic amount. Widow or widower with a disability aged 50 through 59 — 71½%. Widow or widower, any age, caring for a child under age 16 — 75%.

How is a death benefit calculated?

Amount Of Death Benefit Needed Start by taking the income earned by the insured, calculate the total amount that would be lost if the insured died today and assume he/she will earn the same amount until retirement, and add burial and grieving costs such as lost work time.

What is the cash value of a $10000 life insurance policy?

So, the face value of a $10,000 policy is $10,000. This is usually the same amount as the death benefit. Cash Value: For most whole life insurance policies, when you pay your premiums some of that money goes into an investment account. The money in this account is the cash value of that life insurance policy.

Do beneficiaries pay taxes on life insurance policies?

Generally speaking, when the beneficiary of a life insurance policy receives the death benefit, this money is not counted as taxable income, and the beneficiary does not have to pay taxes on it.

What is the difference between life insurance and death benefit?

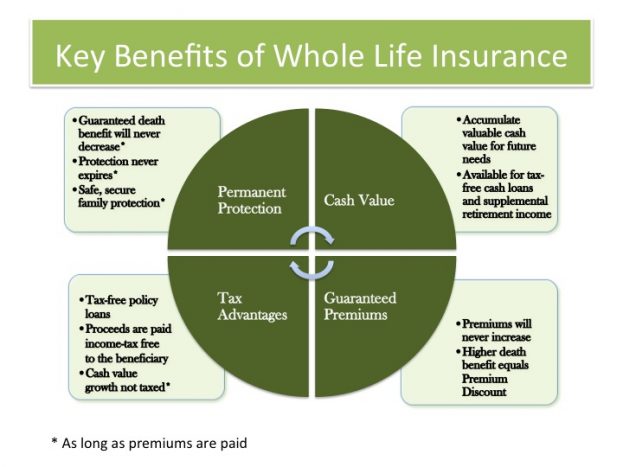

The death benefit is money that's paid to your beneficiaries when you pass away. Cash value is a separate savings component that you may be able to access while you're still alive. ¹ Permanent life insurance lasts from the time you buy a policy to the time you pass away, as long as you pay the required premiums.

What is the most common payout of death benefits?

lump-sum payoutThere are two common distributions. A lump-sum payout means that the entirety of the policy will be paid upfront. This is the most common and is used as the default for most policies. You can also choose for the money to be paid in installments, as an annuity.

Who gets the 255 death benefit?

Only the widow, widower or child of a Social Security beneficiary can collect the $255 death benefit, also known as a lump-sum death payment. Priority goes to a surviving spouse if any of the following apply: The widow or widower was living with the deceased at the time of death.

Who claims the death benefit?

Who reports a death benefit that an employer pays? That depends on who received the death benefit. A death benefit is income of either the estate or the beneficiary who receives it.

Why do you get death benefits on life insurance?

Most likely, this death benefit payout is why you’re buying your life insurance policy in the first place — to ensure that your loved ones don’t financially suffer if you die unexpectedly.

What is death benefit?

The death benefit is the tax-free payout your beneficiaries receive if you die; it's essentially what you're paying for when you sign up for life insurance coverage. Life insurance protects your loved ones from the risk of losing the financial support you provided when you die. If you’re covered, the life insurance company pays your beneficiaries ...

What happens if you die on a life insurance policy?

If you buy a $500,000 life insurance policy, that means the life insurance company will pay the entire $500,000 life insurance death benefit to your beneficiaries if you die while the policy is active (with some rare exceptions ). The amount of coverage you need is the largest factor in determining your premium payments, ...

What happens to an annuity if you die?

If you die while your policy is in force, it is paid out to your beneficiaries as a tax-free lump sum or annuity. The death benefit can range from a few thousand dollars to millions of dollars and the exact amount you should purchase is contingent on your dependents’ needs and your financial circumstances.

What is the death benefit amount paid out?

The death benefit amount paid out is the coverage amount you choose when you buy your policy. If you buy a $1 million life insurance policy, your beneficiaries will receive a $1 million lump sum.

How long does a death benefit payout last?

Contestability. The payout can be delayed if the death occurred during the contestability period, which lasts for two years after the policy is put in force. During this time, the life insurance company reserves the right to dispute or investigate any death benefit claim.

Why is it important to speak to a licensed agent about allocating the right sum for the life insurance death benefit?

Because your loved ones’ financial health is at stake, it’s important to speak to a licensed agent about allocating the right sum for the life insurance death benefit. If you’re able to work with a financial adviser and lay out a strategy for them as to how to spend the death benefit, all the better. → Learn more about how to spend the life ...

How much of life insurance death benefit can you get?

If you’re one of four beneficiaries, that doesn’t automatically mean you’ll get one quarter of the death benefits . The policyholder can allocate different percentages to different beneficiaries.

What is a death benefit and how does it work?

To start, let’s define death benefit: It’s the money – lump sum or otherwise – that gets paid to your beneficiaries if you die while your life insurance policy is in effect. Whether you’re buying life insurance, or you’re filing a claim on a life insurance policy, there are a few things you need to know about beneficiaries:

How to find out if you are a beneficiary of life insurance?

If you believe you are named as a life insurance beneficiary, check online with the National Association of Insurance Commissioners' Life Insurance Policy Locator Service, which searches a database of known policies from participating companies. However, not everyone will get an answer: Life insurance companies will respond to the request only if they have reason to believe there is a policy in the name of the deceased, and you are entitled to death benefits as a designated beneficiary, or authorized to receive information.

How long does it take to get death benefits?

Once the insurance company has your claim, they will verify the information and likely pay out death benefits within 30-60 days of the date the claim was filed. You’ll typically be given a choice of getting your payout in one of 3 different ways: 1. A lump sum payment.

What does it mean when someone says they have $100,000 in life insurance?

It’s the primary reason to get life insurance, and how policies are almost always described: when someone says they have a $100,000 policy, it really means they have $100,000 worth of death benefit insurance.

What is the form to fill out for death certificate?

The insured’s death certificate. While every company’s process varies somewhat, you’ll basically have to fill out a claims form called a “Request for Benefits” and provide a copy of the death certificate. If you are in touch with the insured’s insurance agent, they can help you through the claims process.

Why do you name someone else as a beneficiary?

In fact, there are many reasons for naming someone other than your spouse or children as beneficiaries, including: You want to leave money to care for other family members, such as parents or a sibling. You could leave money to a family-run business to help ensure continuity of operations after you’re gone.

What is the death benefit of life insurance?

If you’re familiar with life insurance, you might know that beneficiaries receive a payout when the policyholder passes away. This is known as the “death benefit” — and if you’re a beneficiary, you’ll need to take steps to claim it.

How much is the death benefit of a life insurance policy?

In most cases, the death benefit is equal to the face value of the policy. For example, if you take out a $250,000 life insurance policy, your beneficiaries will receive $250,000 when you die. You can nominate multiple beneficiaries, and allocate how much money should go to each.

How can I claim a death benefit?

When a policyholder dies, it’s up to the beneficiary to file a claim . The insurance company has no obligation to notify the beneficiary and let them know they’re owed a payout.

When am I eligible to receive a death benefit?

If you’re listed as a beneficiary on a life insurance policy, you’re entitled to the death benefit. The policy specifies the amount of money you’ll receive, and when it will be paid out.

When is the death benefit paid out?

Most insurers pay death benefits a week or two after approving a claim — but some take as long as 60 days.

What happens when a policyholder dies?

When a policyholder dies, it’s up to the beneficiary to file a claim. The insurance company has no obligation to notify the beneficiary and let them know they’re owed a payout. Contact the insurance company to inform them of the policyholder’s death.

What happens if an insurer discovers false information?

If the insurer discovers false information while investigating a claim, it has the right to decrease the death benefit — or deny it altogether. If it chooses to decrease the death benefit, it’ll typically subtract the premiums the policyholder would have paid had they been truthful in their application. The policyholder adjusted the death benefit. ...

What is death benefit?

Death benefits, in a nutshell, are the dollar value of the life insurance policy you’ve taken out. Let’s say you purchase a life insurance policy for $500,000, then when you pass away, your beneficiaries will receive $500,000.

What happens when insurance companies adjust the death benefit?

This means the insurance company will recalculate what the policyholders premiums should have been and adjust the payout to reflect this new information.

When Do Death Benefits Payout?

Then, if the claim is approved, the funds are released – usually, it takes 14-60 days – for the beneficiaries to receive the death benefit payout.

What happens when you buy a life insurance policy for $500,000?

When you purchase your life insurance policy for $500,000, your beneficiaries will receive the full $500,000 as a lump sum payment, in trust or as annuities upon your passing. Ultimately, as the policyholder, you have the freedom to structure the payout as you wish.

What is the function of life insurance?

One of the primary functions of life insurance is providing your family with a death benefit when you pass away. Think of death benefits as a tax-free payout from your insurance company to your beneficiaries—so long as your premiums are up-to-date.

What happens to the estate if you pass without a will?

Heirs: If the policyholder were to pass without a will, the estate goes to the heirs while death benefits go to the designated beneficiaries.

Why do we need life insurance?

Life insurance is a means of providing for our loved ones without us being there, so don’t neglect to buy life insurance if you want to continue providing for your family after you’ve gone.

What is death benefit?

A death benefit is a sum of money paid out to the beneficiary or beneficiaries of a life insurance policy, as long as the insured died while the policy was in effect. The death benefit is the primary purpose of buying life insurance coverage; it’s what your premium payments cover throughout the life of your policy. Ads by Money.

How long does it take to get a death benefit from life insurance?

Life insurance companies typically take up to a month to review a claim before paying out the death benefit. They may request further documentation.

Why might a life insurance claim be denied?

According to a spokesperson for the American Council for Life Insurers (ACLI), less than 0.5% of life insurance claims were disputed at the end of 2019. Although it is not common for claims to be denied, there’s a variety of reasons why your death claim might be rejected.

What happens if a life insurance policy is lapsed?

A lapsed policy. For a life insurance policy to pay out, the policy must be in force, meaning the policyholder was actively making payments to it. If they neglected to make payments and the grace period expired, the policy could lapse, and the death benefit claim could be denied.

How does life insurance work?

How do death benefits work? Life insurance pays out a tax-free death benefit if your policy is active when you die. There are several different types of life insurance policies, but the main categories are term life insurance — the more affordable option — and permanent life insurance.

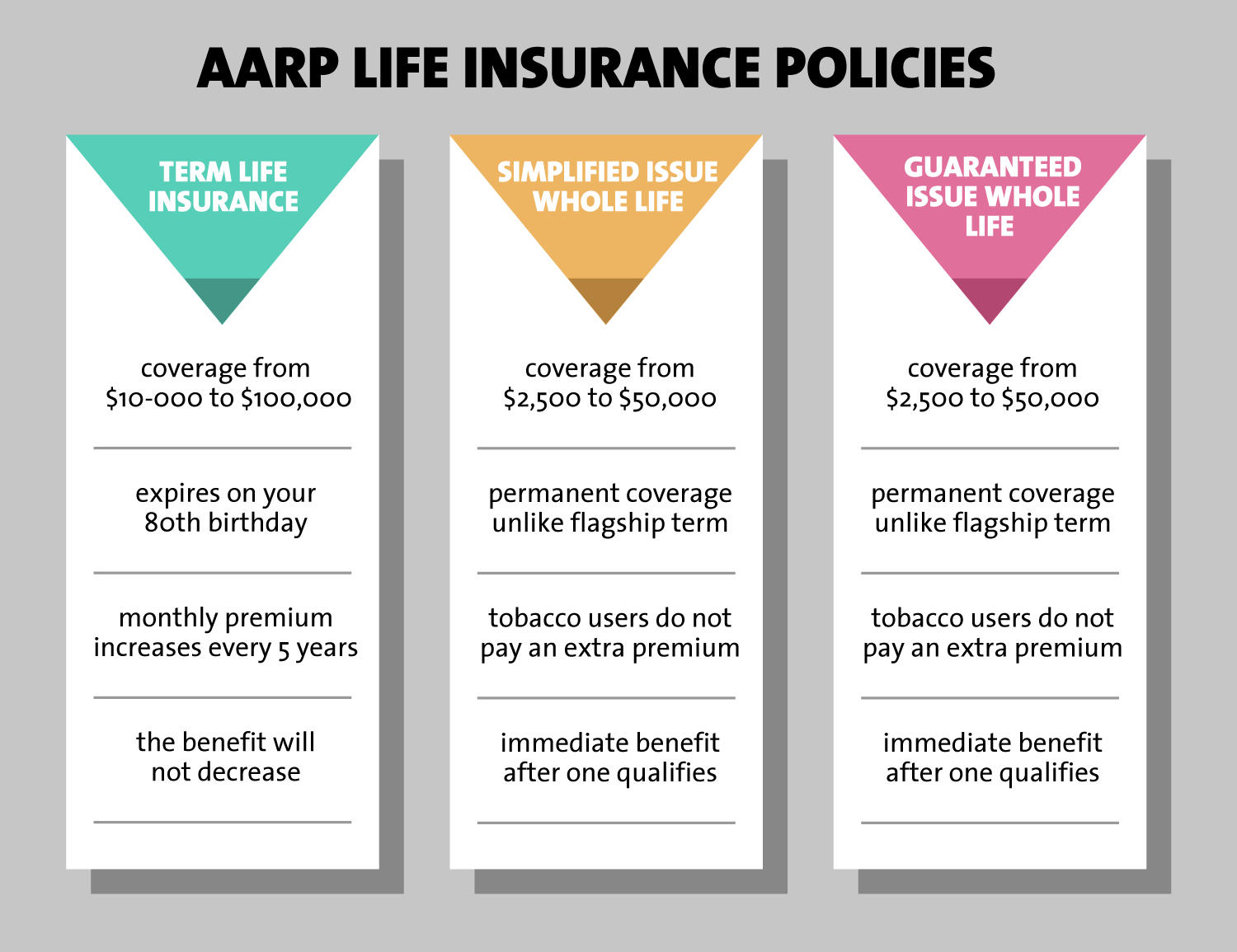

How long does term life insurance last?

Term Life Insurance. Term life insurance policies are in force for a set period or term, which typically range in length from 10 to 30 years. If the insured dies within the policy term, the insurer pays out a death benefit equal to the policy’s face value.

How long does it take to receive death benefit?

The death benefit is invested in an annuity account. Choose direct deposit or check and receive your funds within 30-60 days after processing. Receive monthly or annual payments for 10 to 30 years. The full death benefit is tax-free.

What are the disadvantages of life insurance?

A big disadvantage is the price. Guaranteed issue life insurance is among the most expensive kinds of life insurance. There are also limited payouts available, sometimes no more than $25,000. Graded death benefits are another disadvantage.

What are the advantages of a guaranteed issue life insurance policy?

The key advantages of a guaranteed issue life insurance policy are that you can qualify for a policy regardless of your health, there is no medical exam and the application process is super quick and convenient.

What happens to the insurance company when you pass away?

The graded death benefit reduces risk for the insurance company. If severely ill people buy policies and pass away within two or three years, the insurance company won’t have to pay the full death benefit to beneficiaries.

What is graded death benefit?

Graded death benefits are usually part of guaranteed issue life insurance policies. If you cannot qualify for a traditional life insurance policy because of your health, you may be looking at a guaranteed issue policy.

What happens if you pass the time limit for a graded death benefit?

Once you pass the time limit for a graded death benefit, your beneficiaries will receive the full coverage amount of the life insurance policy.

How old do you have to be to get life insurance?

Many insurance companies that offer these policies won’t sell new policies to you after age 80, and have a minimum purchase age between 40 and 55.

Can you be turned down for life insurance?

You can’t be turned down for a guaranteed issue life insurance policy, so it can be a good fit if you’re in very poor health and wouldn’t qualify for other life insurance, but be aware of how a graded death benefit works.

What Is Life Insurance?

A life insurance policy is a contract between you (the policyholder) and an insurance company. In exchange for paying regular premiums, the insurance company pays a death benefit to your beneficiaries if you die. Life insurance coverage provides a financial safety net, and it could replace your wages or be used to pay off the mortgage or college costs for the kids.

How long does life insurance last?

According to the Insurance Information Institute, it pays if you die during the policy's term, which is usually from one to 30 years. 1 Once the term expires, you can renew it for another term, covert the policy to permanent coverage, or allow the policy to terminate. On the other hand, whole life insurance pays a death benefit whenever you die, ...

What happens if you lie on your life insurance application?

If you lie on your application, your insurer could refuse to pay out to your beneficiaries when you die. Life insurance policies cover suicide, but only if a certain amount of time has passed since buying the policy. If you die participating in a risky hobby, your insurer may or may not pay benefits, depending on your policy's details.

What happens if you lie on your insurance?

Life insurance companies can withhold death benefits if you lie on your application (that's insurance fraud, by the way). For example, the insurer can cancel your policy, and your beneficiaries would lose out on benefits, if you lie about your: 1 Family health history 2 Medical conditions 3 Alcohol and drug use 4 Risky activities 5 Travel plans

What happens if you die in a hobby?

The "Slayer Rule" prevents a death benefit payout to your beneficiary if they murder you or are closely tied to your murder.

What happens if you die from natural causes?

In general, if you die due to natural causes, an illness, or an accident, your designated beneficiaries will get the life insurance payout. Here's a quick rundown of the types of deaths that are covered under life insurance policies:

Do you have to designate beneficiaries for death insurance?

It's essential to designate primary and contingent beneficiaries to receive the insurance death benefit in the event of your untimely death. Otherwise, the benefits are subject to probate, and they ultimately may not end up where you intended.