Who benefits from a pension after death?

Under current law, we recognize these wartime periods to decide eligibility for pension benefits:

- Mexican Border period (May 9, 1916, to April 5, 1917, for Veterans who served in Mexico, on its borders, or in adjacent waters)

- World War I (April 6, 1917, to November 11, 1918)

- World War II (December 7, 1941, to December 31, 1946)

- Korean conflict (June 27, 1950, to January 31, 1955)

Does the benificiary pay taxes on death benefit?

The federal government does not impose an inheritance tax. The beneficiary pays inheritance taxes at the state level if the decedent held it or died in one of the six states that have an inheritance tax. As of 2021 Nebraska, Iowa, Kentucky, Pennsylvania, New Jersey and Maryland collect inheritance taxes.

Do you have to pay taxes on death benefit?

In most cases, your beneficiary won't have to pay income taxes on the death benefit. But if you want to cash in your policy, it may be taxable. If you have a cash-value policy, withdrawing more than your basis (the money it's gained) is taxable as ordinary income.

Do pensions pay after death?

We say generally because there is a condition which needs to be met for the payments to be free of income tax – the pension fund has to be paid to your beneficiaries within two years of your death. This can be confusing as it does not mean that they have to take all of the money out of your pension.

Do beneficiaries pay taxes on pensions?

With a pension, people pay income taxes when they withdraw the money in retirement or their heirs pay income taxes when they inherit it. The income tax rates that apply are those that apply at the time of the withdrawal or inheritance.

Are pension lump sum death benefits taxable?

Taxes - Lump Sum Benefit The death benefit is not life insurance and is taxable. The payment may be paid in a direct rollover or directly to the beneficiary.

Are death benefits paid to a survivor beneficiary taxable?

These retirement contributions the deceased employee (made bi-weekly via payroll deduction to the FERS Retirement and Disability Fund) were made with after-taxed dollars. If a FERS spousal survivor annuity is also paid, then all of the special death benefit is taxable.

How are pension survivor benefits taxed?

They are not taxable when the member receives them as a refund or pension or when the member's beneficiary(ies) receives them as a death benefit. tax-deferred member contributions and the interest are taxable. The income tax treatment is the same as that described in subparagraph 1(c) above.

When a person dies what happens to their pension?

The deceased person may have been entitled to pension benefits from a private company, government agency, or union. Some pensions end at death, but many pensions provide for payments to a surviving spouse or dependent children. Survivors may be entitled to part of the payments the person would have received.

How much tax do I pay on a death benefit?

Generally speaking, when the beneficiary of a life insurance policy receives the death benefit, this money is not counted as taxable income, and the beneficiary does not have to pay taxes on it.

Is pension to widow taxable?

Commuted pension received by family members is exempt from tax. However, in case of uncommuted pension received by family members, a sum equal to 33.33% of such income or ₹ 5,000, whichever is less, is exempted from tax. So, if a widow receives a pension of ₹ 0,000 a month or ₹ .

What are the taxes on pension death benefits?

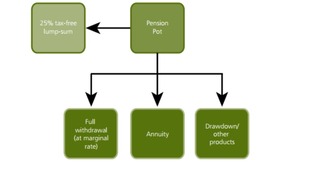

There are 4 taxes pension death benefits can be subject to: income tax. lifetime allowance charge. inheritance tax. special lump sum death benefits charge. These mostly apply regardless of whether death benefits are paid as a lump sum, beneficiary income drawdown or beneficiary annuity. In this article we look at each tax in turn.

When did pension death benefits depend on income tax?

Since 6 April 2015, the income tax situation of pension death benefits has depended on the age of the deceased member or the deceased beneficiary (in the case of someone who dies while entitled to a beneficiary income drawdown plan).

What is a special lump sum death benefit?

Special lump sum death benefits charge. If death benefits are subject to income tax and are paid as a lump sum to a trust, a 45% tax charge applies. This is called a special lump sum death benefits charge. Any payments made to the beneficiaries from the trust will be subject to income tax but the tax payable can be offset against ...

What is lifetime allowance?

Lifetime allowance. The payment of death benefits can be a benefit crystallisation event or several benefit crystallisation events. These range from paying death benefits as lump sums ( BCE 7) to paying them as beneficiary drawdown ( BCE 5C) or paying them as a beneficiary annuity ( BCE 5D ).

How to avoid inheritance tax?

To avoid inheritance tax, the member can opt to have the death benefits paid at the discretion of the scheme administrator. As the member isn’t in control of who the death benefits are paid to, they’re deemed not to form part of their estate and so aren’t liable for inheritance tax. The member can still state who they’d like the death benefits to be paid to and in most cases that’s who will receive them but the final say lies with the scheme administrator. Most people are happy to give up a little bit of control in order to avoid inheritance tax knowing their choice of beneficiary will be used as a guide by the scheme administrator whose choice of beneficiary has to be justifiable. The scheme administrator will only fail to follow the member’s wishes if there’s a good reason.

How much is Leanne's death benefit worth?

The death benefits are worth £100,000. If Leanne takes the benefits as a lump sum, her taxable income becomes £140,000 and her tax bill is:

How long after Sean died would he have to pay taxes?

In the above example if the death benefits were paid out more than 2 years after the scheme administrator knew of Sean’s death, the death benefits would have been subject to income tax despite Sean having died at age 64.

What happens to a participant in a retirement plan when he dies?

When a participant in a retirement plan dies, benefits the participant would have been entitled to are usually paid to the participant’s designated beneficiary in a form provided by the terms of the plan (lump-sum distribution or an annuity).

What to do when a spouse dies in a retirement plan?

When a plan participant dies, the surviving spouse should contact the deceased spouse’s employer or the plan’s administrator to make a claim for any available benefits. The plan will likely request a copy of the death certificate. Depending upon the type of plan, and whether the participant died before or after retirement payments had started, the plan will notify the surviving spouse as to:

What is pension plan?

Pension plans are a type of retirement plan that requires an employer to make contributions to a pool of funds set aside for a worker's future benefit. The pool of funds is invested on the employee's behalf, and the earnings on the investments generate income to the worker upon retirement. Pension plan options typically offer a lump-sum ...

What are the different types of pension plans?

Types of Pensions. There are two main types of pension plans: defined-benefit and defined-contribution . A defined-benefit plan is what people normally think of as a "pension.". It is an employer-sponsored retirement plan in which employee benefits are computed using a formula that considers several factors, such as length ...

How to notify a spouse of a death?

"When a plan participant dies, the surviving spouse should contact the deceased spouse’s employer or the plan’s administrator to make a claim for any available benefits. The plan will likely request a copy of the death certificate. Depending upon the type of plan, and whether the participant died before or after retirement payments had started, the plan will notify the surviving spouse as to: 1 the amount and form of benefits (in other words, lump sum or installment payments under an annuity); 2 whether death benefit payments from the plan may be rolled over into another retirement plan; and 3 if a rollover is possible, the method and time period in which the rollover must be made." 3

What is a period certain annuity?

Period Certain Annuity. A period certain annuity option allows the customer to choose how long to receive payments. This method allows beneficiaries to later receive the benefit if the period has not expired at the date of the member's death.

Why is defined benefit called defined benefit?

It is called "defined benefit" because employees and employers know the formula for calculating retirement benefits ahead of time, and they use it to set the benefit paid out. The employer typically funds the plan by contributing a regular amount, usually a percentage of the employee's pay, into a tax-deferred account.

Can a spouse be a beneficiary of a joint life plan?

If the plan member is married with a joint-life payout option, the default beneficiary is automatically the member's spouse unless the spouse waives that option. The spouse would need to certify in writing via a spousal consent or spousal waiver form that they are choosing not to receive survivor benefits. 4 5 It may need to be notarized. If done properly, this allows the member to designate another beneficiary, such as a child. If the plan member is not married, they may designate another beneficiary.

Can you continue to receive pension benefits if your parents retire?

Assuming your parent elected a period certain pension option for payment at retirement and named you as beneficiaries, you and your siblings would be entitled to the continuing payments until the period expires.

What happens to your life insurance when your spouse dies?

When your spouse dies, whatever life insurance payments or other death benefits has set up become available to you. Depending on the circumstances and terms, it may also pay off for the IRS. Many employers offer death benefits as part of the company's retirement planning, but some of the money may go to the government instead of you.

Is there a tax on death benefits?

If the accident policy kicks in because it covered your spouse's accidental death, the same rules apply as for life insurance. If all you get is the flat death benefit, with no interest, there's no tax.

Is life insurance taxable?

Life Insurance. The payout from insurance when someone dies may be taxable. If your spouse named you as beneficiary of a $150,000 policy, the $150,000 is tax free. If the policy earns interest, however, any extra money you get above the face value is taxable income.

Is a survivor benefit taxable?

There are many other types of survivor benefits your spouse's employer may pay you besides those in the retirement plan. If your spouse had any wages due when he died, for instance, you probably get the money. In that case, it's as taxable to you as it would have been to your spouse.

Is an annuity taxable if you have a pension?

Pension and Annuity. Death benefits bought under a pension or an annuity work much the same as life insurance. They're not taxable unless they exceed the value of the contract. If the death benefit is more than that, then the IRS gets a cut. The number-crunching guidelines for figuring this one are in Publication 575.

What is lump sum death benefit?

A lump sum death benefit payment is a lump sum paid from a pension scheme following the death of the member or beneficiary.

Who is receiving lump sum death benefits?

the special lump sum death benefits charge if paid to: someone other than an individual. an individual who is receiving the payment in their capacity as a trustee, personal representative, director of a company, partner in a firm or member of a limited liability partnership. If the lump sum was paid to a trust, and then pays it to a beneficiary, ...

Can you deduct commutation death benefits?

For payments other than trivial commutation lump sum death benefits, the amount you deduct depends on who you make the payment to. You should deduct either: Income Tax using the emergency tax code if paid directly to an individual (they may be able to reclaim a repayment if they’ve paid too much tax) the special lump sum death benefits charge ...

Can a beneficiary claim back a lump sum?

If the lump sum was paid to a trust, and then pays it to a beneficiary, the beneficiary can claim back some or all of the tax.

How long do you have to live on a pension transfer?

How to transfer a pension? Where a transfer between pension schemes is instructed and you were in ill health, it would be necessary to survive for a period of 2 years after the date of the transfer for the pension to automatically be exempt from inheritance tax.

How to inform trustees of pension?

You can inform the trustees of your pension who you would like to benefit from your pension by completing an “expression of wish” or “death benefit nomination” form.

When did pension freedom start?

The introduction of “Pensions Freedom” during 2015 has given you the control and flexibility to pass on your defined contribution pension savings to any beneficiaries of your choice without being subject to inheritance tax.

Is pension a savings vehicle?

Historically, Pensions have been seen as a tax efficient savings vehicle to provide YOU with income in retirement. However, more recently investors are looking closely at how their income in retirement is structured, especially where there is potentially an Inheritance Tax liability on the assets that make up your taxable estate. ...

Do pensions fall outside of estate?

Savings within most modern defined contribution pension products fall outside of your “taxable estate” and are therefore not subject to inheritance tax on death. There are exceptions and you should check that your existing pension savings are positioned correctly to benefit from these tax advantages on death.

Do defined contribution pensions have inheritance tax?

As mentioned earlier, savings within most modern defined contribution Pension products fall outside of your “taxable estate” and are therefore not subject to Inheritance Tax on death. This makes them an extremely attractive vehicle for passing on wealth to future generations under current legislation.

Do pension funds get taxed after death?

It is important to remember that the trustees of your Pension must retain discretion over who ultimately receives the value of your Pension after your death, for the fund to be exempt from Inheritance Tax.

How long after death do you have to pay taxes on a lifetime allowance?

You will not pay lifetime allowance tax charge if you got the pot more than 2 years after the provider was told about the death.

How long do you get paid after a pension provider dies?

you’re paid more than 2 years after the pension provider is told of the death. they had pension savings worth more than £1,073,100 (the ‘lifetime allowance’) they died before 3 December 2014 and you buy an annuity from the pot.

What happens if you buy an annuity from the pot?

If you buy an annuity from the pot, the provider takes Income Tax off payments before you get them.

How long do you have to pay taxes on pension pot?

Income Tax deducted by the provider. You may also have to pay tax if the pension pot’s owner was under 75 when they died and any of the following apply: you’re paid more than 2 years after the pension provider is told of the death.

How long do you have to tell HMRC about your death?

The person dealing with the estate must tell HMRC within 13 months of the death or 30 days after they realise you owe tax (whichever is later).

Do you pay taxes on a pot after death?

You pay tax if the pot’s owner was under 75, and it’s more than 2 years after the provider is told of their death when you get either: an annuity or drawdown fund from an ‘untouched’ pot (the person who died did not take any money from it) In both cases, the provider will deduct Income Tax before you’re paid.

Do you have to pay taxes on a pension you inherit?

Tax on a private pension you inherit. You may have to pay tax on payments you get from someone else’s pension pot after they die. There are different rules on inheriting the State Pension.

When is an annuity distribution taxed?

If a beneficiary receives a lump sum amount from an employer-sponsored variable annuity after the owner’s death, the distribution is usually taxed only if it exceeds the unrecovered cost of the annuity contract. If you decide to receive annuity payments instead of a lump sum, these distributions are only subject to tax when exceeding ...

Is a company retirement plan taxable?

There are a few factors that determine whether or not death benefits from a company retirement plan are taxable, including the kind of benefits and the relationship between the beneficiary and the deceased.

Can a beneficiary leave a 401(k)?

If the beneficiary is not the surviving spouse, she may leave the 401 (k) with the plan provider if the plan allows for this. Such heirs may also roll over the funds into an inherited IRA. Depending on the 401 (k) plan, this heir may have to remove the entire amount in the account within five years or take a lump sum distribution.

Can a surviving spouse withdraw from 401(k)?

The surviving spouse may also leave the funds in his late spouse’s 401 (k) plan and begin making withdrawals at the time in which the deceased would have turned 70 ½, with the withdrawals again subject to tax based on his income tax bracket.

Is a pension plan taxable income?

If the beneficiary begins receiving death benefits from a pension plan, t his amount is usually taxable as ordinary income. Pension plan beneficiaries usually receive a percentage of the amount of the deceased’s plan benefit, often about two-thirds.

Is a death benefit plan taxable?

Whether death benefits from a company’s retirement plan are taxable for the beneficiary depends on the type of death benefit as well as the beneficiary’s relationship to the deceased. Company death benefit plans do not go through probate, as the late account owner designated beneficiaries at the time of the account's establishment.

Do 401(k) plans have to be tax free?

Evaluating 401 (k) Plans. In a 401 ( k), earnings accumulate tax free until the owner of the account begins making withdrawals. In retirement, most people find themselves in a lower tax bracket than during their working years. A beneficiary inheriting a 401 (k) would similarly owe tax on distributions. If the beneficiary is a surviving spouse, he ...

What is the death benefit receivable?

The amount of the death benefit receivable from an annuity may be the entire amount left in the contract at the time of the policyholder’s death. In the case where the annuitant has made any withdrawals, the same amount and any applicable fees and/or charges are deducted from the death proceeds.

What happens to an annuity when the holder of the contract passes away?

When the holder of an annuity contract passes away, the money and the death benefit available from the annuity come into play. Many annuity products come with the provision for the annuity holder to include a death benefit for a beneficiary, which they choose while setting up the contract.

What is an annuity?

A simple way to think of an annuity is to refer to it as an insurance product that offers a certain income benefit, backed by contractual guarantees. It can be utilized as a component of a retirement benefit plan.

Is an annuity death benefit taxable?

As the annuity death benefit is taxable, you may also consider purchasing a life insurance policy in order to cover your estimated tax amount. This is probably one of the best ways for you to ensure that you have a higher amount for your own use.

Is death benefit taxable if an annuitant dies?

When the annuitant passes away, the fate of the available death benefit depends on who the beneficiary is. This death benefit is not taxable as long as it remains inside the annuity.

Is an annuity taxable?

The proceeds from an annuity death benefit are taxable when they are received by the beneficiary. In the case where the recipient is a surviving spouse, he or she can initiate certain measures to defer the payment or taxes on the amount received.

Do annuities have a death benefit rider?

There are some types of annuities that offer a guaranteed death benefit to the beneficiary no matter the amount left over in the contract. However, in order to enjoy this death benefit rider, the annuity owner will need to pay an annual fee.