Claiming Early Social Security Retirement Benefits

| BIRTH YEAR | FULL RETIREMENT AGE | BENEFIT |

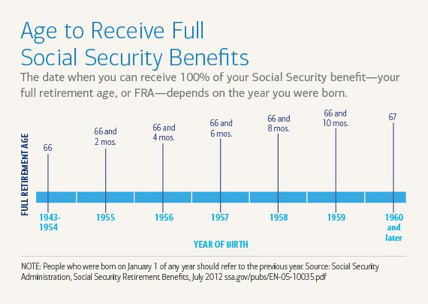

| 1957 | 66 years, 6 months | $725 |

| 1958 | 66 years, 8 months | $716 |

| 1959 | 66 years, 10 months | $708 |

| 1960 and later | 67 years | $700 |

Why do so many people claim social security at 62?

The simplest explanation for why so many people claim Social Security at 62 is because they can't claim benefits any earlier. Many people count the days until they can get benefits because they need this money to leave the workforce or to survive comfortably if they've already been forced out of a job.

When taking social security at 62 could be wise?

You can begin withdrawing from Social Security at age 62, but there are some good reasons to wait. Your benefits will be reduced until your full retirement age if you make more than the annual earnings limit. If your benefits won't be reduced, or if you don't have any other accounts to withdraw from, you might need to begin withdrawing at age 62.

How much does social security go up each year after age 62?

The actual year-over-year percentage gain for ages 62 to 70 are shown in the following table. Those gains range from 6.5 percent (claiming at 70 rather than 69) to 8.4% percent (claiming at 64 rather than 63).

What is the maximum Social Security benefit at age 62?

You cannot collect your personal SS retirement benefit until you are at least 62 years old, but if you claim at that age ... your maximum benefit would be 24% more than it would be at your FRA. You have an 8 year window to claim your Social Security ...

What is the average Social Security benefit at age 62?

$2,364At age 62: $2,364. At age 65: $2,993. At age 66: $3,240. At age 70: $4,194.

How do I find out how much Social Security I would get at 62?

You can also get basic benefit estimates by calling the Social Security Administration at 800-772-1213.

How much would I receive if I retire at 62?

A single person born in 1960 who has averaged a $50,000 salary, for example, would get $1,349 a month by retiring at 62 — the earliest to start collecting. The same person would get $1,927 by waiting until age 67, full retirement age.

Can I draw Social Security at 62 and still work full time?

Can You Collect Social Security at 62 and Still Work? You can collect Social Security retirement benefits at age 62 and still work. If you earn over a certain amount, however, your benefits will be temporarily reduced until you reach full retirement age.

Is Social Security based on the last 5 years of work?

A: Your Social Security payment is based on your best 35 years of work. And, whether we like it or not, if you don't have 35 years of work, the Social Security Administration (SSA) still uses 35 years and posts zeros for the missing years, says Andy Landis, author of Social Security: The Inside Story, 2016 Edition.

How much will I get from Social Security if I make $30000?

1:252:31How much your Social Security benefits will be if you make $30,000 ...YouTubeStart of suggested clipEnd of suggested clipYou get 32 percent of your earnings between 996. Dollars and six thousand and two dollars whichMoreYou get 32 percent of your earnings between 996. Dollars and six thousand and two dollars which comes out to just under 500 bucks.

How do I find out how much Social Security I will get?

Benefit Calculators (En español) The best way to start planning for your future is by creating a my Social Security account online. With my Social Security, you can verify your earnings, get your Social Security Statement, and much more – all from the comfort of your home or office.

Is it better to take Social Security at 62 or 67?

The short answer is yes. Retirees who begin collecting Social Security at 62 instead of at the full retirement age (67 for those born in 1960 or later) can expect their monthly benefits to be 30% lower. So, delaying claiming until 67 will result in a larger monthly check.

Although you'll receive reduced checks by claiming early, you can still receive thousands of dollars per month

The age at which you file for Social Security benefits will have a major impact on the amount you receive each month. While you can receive larger monthly payments by delaying benefits, many workers choose to file as early as possible at age 62. That can be a smart strategy in many cases, and there are several advantages to claiming early.

How the length of your career affects your benefits

One of the most important factors when it comes to your benefit amount is the number of years you've worked. Most people become eligible for Social Security retirement benefits once they've earned income for 10 years, but you'll need to work for at least 35 years to receive the maximum benefit amount.

How much you'll have to earn to reach the maximum benefit amount

Your income is another crucial factor in reaching the highest benefit amount. The more you're earning, the more you'll be eligible to collect in benefits -- up to a certain point.

What if your earnings are falling short?

If you're earning enough to reach the maximum benefit amount, that's fantastic. But the average worker will struggle to reach the income limits, and not everyone can afford to work 35 years before claiming.

Premium Investing Services

Invest better with the Motley Fool. Get stock recommendations, portfolio guidance, and more from the Motley Fool's premium services.

How much will Social Security increase if you wait to claim?

Waiting to claim your Social Security benefit will result in a higher benefit. For every year you delay your claim past your FRA, you get an 8% increase in your benefit. That could be at least a 24% higher monthly benefit if you delay claiming until age 70. But, make sure to evaluate your decision based on how much you've saved for retirement, ...

What are the factors that affect Social Security?

Plus, guaranteed monthly income is nice to have. Health status, longevity, and retirement lifestyle are 3 key factors that can play a role in your decision when to claim your Social Security benefits.

What is the reduction for claiming your own FRA?

If claiming spousal benefits provides more, claiming before your FRA on a spouse's record means you'll lose even more than claiming on your own record—the benefit reduction for a spouse is up to 35% while the reduction for claiming your own benefit is up to 30% .

What is the downside of claiming early?

The downside of claiming early: Reduced benefits. Consider the following hypothetical example. Colleen is 62 as of 2022. If Colleen waits until age 67 (her FRA) to collect, she will receive approximately $2,000 a month. However, if she begins taking benefits at age 62, she'll receive only $1,400 a month.

How much will Social Security be at 62?

Your monthly benefit check will permanently decrease by 20-30%. This chart illustrates how much an estimated $1,000 monthly benefit payment will be worth if you start taking it at age 62, relative to your Full Retirement Age.

Can you defer retirement benefits?

Conversely, you can also defer retirement benefits. This typically increases your annual payout by about 8% for each year you delay beyond your Full Retirement Age, to a maximum of age 70.

What happens if you file for Social Security at 62?

By filing at 62, or any time before you reach full retirement age, you forfeit a portion of your monthly benefit. If you were born in 1960 or later, for instance, filing at 62 could reduce your monthly payment by as much as 30 percent. AARP’s Social Security Benefits Calculator can provide more details on how filing early reduces benefits.

When can I collect Social Security if I was born on the first day of the month?

For example, if you were born on Oct. 1 or 2, 1959, Social Security considers you to be 62 as of Sept. 30 or Oct. 1, 2021.

When will Social Security start in 2021?

For example, if you were born on Oct. 1 or 2, 1959, Social Security considers you to be 62 as of Sept. 30 or Oct. 1, 2021. Your benefits will start in October 2021; you can apply for benefits in June. But if you were born between Oct. 3 and 31, your first full month at 62 is November. If you want to start your benefits as soon as possible, ...

When will I get my unemployment benefits if I was born in October?

There is a one-month lag in the benefit payment. If your birthday is Oct. 1 or 2, you qualify for an October benefit and it will be paid in November. If you were born later in October, your first benefit month is November and you will be paid in December.

How old do you have to be to file for Social Security?

You must be at least age 22 to use the form at right. Lack of a substantial earnings history will cause retirement benefit estimates to be unreliable. Enter your date of birth ( month / day / year format) / /. Enter earnings in the current year: $. Your annual earnings must be earnings covered by Social Security.

What happens if you don't give a retirement date?

If you do not give a retirement date and if you have not reached your normal (or full) retirement age, the Quick Calculator will give benefit estimates for three different retirement ages .

How old do you have to be to use Quick Calculator?

You must be at least age 22 to use the form at right.

What is the benefit estimate?

Benefit estimates depend on your date of birth and on your earnings history. For security, the "Quick Calculator" does not access your earnings record; instead, it will estimate your earnings based on information you provide. So benefit estimates made by the Quick Calculator are rough. Although the "Quick Calculator" makes an initial assumption ...

Benefit Calculators

The best way to start planning for your future is by creating a my Social Security account online. With my Social Security, you can verify your earnings, get your Social Security Statement, and much more – all from the comfort of your home or office.

Online Benefits Calculator

These tools can be accurate but require access to your official earnings record in our database. The simplest way to do that is by creating or logging in to your my Social Security account. The other way is to answer a series of questions to prove your identity.

Additional Online Tools

Find your full retirement age and learn how your monthly benefits may be reduced if you retire before your full retirement age.

When do you start receiving spousal benefits?

Please note that relatively few people can begin receiving a benefit at exact age 62 because a person must be 62 throughout the first month of retirement. Thus most early retirees begin at age 62 and 1 month. Primary and spousal benefits at age 62 .

What percentage of primary insurance does a spouse receive?

If the spouse of a primary begins to receive benefits at his/her normal retirement age, the spouse will receive 50 percent of the primary's primary insurance amount. The table below illustrates the effect of early retirement, for both a retired worker and his/her spouse.

Why is a retired worker called the primary beneficiary?

We sometimes call a retired worker the primary beneficiary, because it is upon his/her primary insurance amount that all dependent and survivor benefits are based.

What age can a spouse file for Social Security?

When a worker files for retirement benefits, the worker's spouse may be eligible for a benefit based on the worker's earnings. Another requirement is that the spouse must be at least age 62 or have a qualifying child in her/his care. By a qualifying child, we mean a child who is under age 16 or who receives Social Security disability benefits.

How much is spousal benefit reduced?

A spousal benefit is reduced 25/36 of one percent for each month before normal retirement age, up to 36 months. If the number of months exceeds 36, then the benefit is further reduced 5/12 of one percent per month.

What is the reduction factor for spousal benefits?

For a spouse who is not entitled to benefits on his or her own earnings record, this reduction factor is applied to the base spousal benefit, which is 50 percent of the worker's primary insurance amount. For example, if the worker's primary insurance amount is $1,600 and the worker's spouse chooses to begin receiving benefits 36 months ...

Can a spouse reduce their spousal benefit?

However, if a spouse is caring for a qualifying child, the spousal benefit is not reduced. If a spouse is eligible for a retirement benefit based on his or her own earnings, and if that benefit is higher than the spousal benefit, then we pay the retirement benefit. Otherwise we pay the spousal benefit. Compute the effect of early retirement ...